Contents

1 IFRS 16 at a glance 2

1.1 Key facts 2

1.2 Key application issues 3

2 Lessee accounting 4

2.1 Lessee accounting model 4

2.2 Initial measurement of the lease liability 5

2.3 Initial measurement of the right-of-use asset 11

2.4 Subsequent measurement of the lease liability 12

2.5 Subsequent measurement of the right-of-use

asset 15

2.6 Recognition exemptions for lessees 17

2.7 Presentation and disclosure 20

3 Lessor accounting 23

3.1 Lessor accounting model 23

3.2 Lease classication 24

3.3 Operating lease model 27

3.4 Finance lease model 28

3.5 Presentation and disclosure 29

4 Lease denition 31

4.1 Overview 31

4.2 Identied asset 32

4.3 Economic benets from using the asset 38

4.4 Right to direct the use 40

5 Separating components 46

5.1 Overview 46

5.2 Identify separate lease components 46

5.3 Identify separate non-lease components 48

5.4 Allocate the consideration 50

5.5 Allocate the variable consideration 53

6 Lease term 56

6.1 Overview 56

6.2 The non-cancellable period 57

6.3 The enforceable period 57

6.4 The reasonably certain threshold 60

6.5 Renewable and cancellable leases 62

6.6 Changes in the lease term 64

7 Lease modications 68

7.1 Denition 68

7.2 Lessee modication accounting 70

7.3 Lessor modication accounting 75

8 Sub-leases 80

9 Sale-and-leaseback 82

Appendix I: List of examples 86

Keeping in touch 88

About this publication 90

Acknowledgements 90

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

The new normal for lease

accounting

IFRS 16 Leases has now been successfully adopted by companies reporting under

IFRS

®

Standards. It is the new normal for lease accounting around the world.

IFRS 16 had a signicant impact on the nancial statements of lessees with

‘big-ticket’ leases, from retailers to banks to media companies. Although lessors

found much that was familiar in IFRS 16, they faced new guidance on a number

of aspects, from separating lease and non-lease components, to more radical

accounting changes for more complex arrangements such as sale-and-leaseback

transactions and sub-leases.

Many implementation challenges have become day-to-day application issues.

Some of these are technical accounting challenges – e.g. identifying which

transactions are or contain leases. Other challenges relate to systems and

processes – e.g. gathering the data required to drive lease accounting and support

the ongoing judgements required to apply IFRS 16.

Some of these challenges could not have been foreseen. The COVID-19 pandemic

has resulted in record numbers of changes to lease agreements. An in-depth

understanding of IFRS 16’s detailed guidance on lease modications is currently

essential, and many lessees have taken advantage of the new practical expedient

for rent concessions.

This publication provides an overview of IFRS 16’s accounting models for lessees

and lessors. It then takes a deeper dive into critical areas such as lease denition

and accounting for lease modications.

If you are looking for a practical overview of IFRS 16, or just a refresher, you’ve

come to the right place. We have included examples and insights to help you

understand the requirements and their impacts on the nancial statements. If you

want to know more, see our detailed publications on lease accounting available at

home.kpmg/ifrs16.

Kimber Bascom

Brian O’Donovan

Marcio Rost

KPMG global IFRS leases leadership team

KPMG International Standards Group

2 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

1 IFRS 16 at a glance

1.1 Key facts

This publication provides an overview of IFRS 16 and how it affects the nancial

statements of the lessee and the lessor. It includes examples and insights.

The publication begins with an overview of the lessee and lessor accounting

models, summarising the impact of IFRS 16 on their respective nancial

statements. To apply their respective models, the lessee and the lessor need

to follow preliminary steps that are discussed in more detail in the subsequent

chapters: identify the lease (see Chapter 4), separate components (see Chapter5)

and determine the lease term (see Chapter 6). The lessee will need to choose

whether to apply the recognition exemptions (see Section 2.6).

The following diagram illustrates the relationships between key elements of the

standard, and shows where each is discussed in this publication.

Many chapters include links to our more detailed guidance. You can also nd more

general guidance on IFRS 16 in Chapter 5.1 in our publication Insights into IFRS

and at home.kpmg/ifrs16.

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

1 IFRS 16 at a glance 3

1.2 Key application issues

1.2 Key application issues

Applying IFRS 16 involves signicant judgements and accounting policy elections

that may impact the recognition of assets and liabilities, and their measurement.

Applying the denition of a lease

Assessing whether an arrangement is, or contains, a lease determines whether

an arrangement is on- or off-balance sheet for a customer. The assessment can be

complex and is required for each new contract. It includes consideration of:

– supplier’s substitution rights: even if the supplier has the right to substitute the

leased asset, there could still be a lease unless the supplier has the practical

ability to substitute the asset throughout the period of use and it would benet

economically from the substitution (see 4.2.3); and

– who takes the relevant decisions that affect the economic benets arising from

the lease asset throughout the lease term: this assessment can be particularly

judgemental when both the supplier and the customer take some decisions, or

many decisions are predetermined (see 4.4.1–2).

Determining the lease term

The assessment of the lease term is a critical estimate and a key input into the

amount of the lease liability for the lessee. For lessees, the lease term also

determines whether a lease is eligible for the recognition exemption for short-term

leases. For lessors, it affects lease classication and income recognition.

– Determining the enforceable period is complex when relevant laws and

regulations in the local jurisdiction create enforceable rights and obligations

in addition to those set out in the written lease agreement. Determining the

broader economic penalties incurred by the lessee and lessor when exercising a

termination right also presents interesting challenges (see Section6.3).

– Determining the lease term for renewable and cancellable leases, including

assessing the enforceable period, was a complex implementation issue on which

the IFRS Interpretations Committee has provided guidance (see Section 6.5).

Lease modications

The guidance on lease modications has been a key area of focus for many

companies due to the economic impact of the COVID-19 pandemic (see

Chapter7).

Key accounting policy choices and exemptions

– A lessee can elect not to apply the lessee accounting model to leases with a

lease term of 12 months or less that do not contain a purchase option (by class

of underlying asset) and leases for which the underlying asset is of low value

when it is new (on a lease-by-lease basis) (see Section 2.6).

– A lessee can elect, by class of underlying asset, to combine each lease

component and any associated non-lease components and account for them as

a single lease component (see Section 5.3).

– A lessee may apply a practical expedient that simplies the accounting for

eligible rent concessions that are a direct consequence of the COVID-19

pandemic (see 7.2.4).

– Both the lessee and the lessor may apply the standard to a portfolio of lease

contracts if certain conditions are met (see Section 5.2).

4 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Lessee accounting

The key objective of IFRS 16 is to ensure that lessees recognise

assets and liabilities for their major leases.

2.1 Lessee accounting model

IFRS 16.22 A lessee applies a single lease accounting model under which it recognises all

leases on-balance sheet, unless it elects to apply the recognition exemptions (see

Section 2.6). A lessee recognises a right-of-use asset representing its right to

use the underlying asset and a lease liability representing its obligation to make

payments.

IFRS 16.47, 49

Is IFRS 16 a pre-tax accounting model?

Yes. IFRS 16 continues to address lessee (and lessor) accounting on a pre-tax

basis, even if tax considerations are often a major factor when a company is

assessing whether to lease or buy an asset, and when a lessor is pricing a lease

contract.

The income tax accounting for lease contracts is in the scope of IAS12 Income

Taxes. The complexities in accounting for income taxes by lessees of on-

balance sheet leases include, for example, how to apply the initial recognition

exemption. The International Accounting Standards Board (the Board) is

expected to issue an amendment to IAS 12 addressing this issue.

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Lessee accounting 5

2.2 Initial measurement of the lease liability

2.2 Initial measurement of the lease liability

2.2.1 Overview

IFRS 16.26 A lessee initially measures the lease liability at the present value of the future

lease payments.

The key inputs to this calculation are asfollows.

When does a lessee rst measure the lease liability?

IFRS 16.A A lessee initially measures the lease liability at the commencement date of the

lease. This is the date on which a lessor makes an underlying asset available for

use by a lessee.

The commencement date should be distinguished from the inception date of

a lease, which is the earlier of the date of the lease agreement and the date of

commitment by the parties to the principal terms and conditions of the lease. A

company assesses whether a contract is, or contains, a lease at the inception

date.

Are lease liabilities nancial liabilities?

IFRS 9.2.1(b) Yes, lease liabilities are nancial liabilities measured in accordance with

IFRS 16 – not IFRS 9 Financial Instruments. However, they are subject to the

derecognition requirements of IFRS 9.

This represents a considerable simplication compared with nancial

instruments accounting in some cases. For example, common features of

lease agreements – e.g. renewal and purchase options – are not accounted

for separately, nor do they have the potential to result in the liability being

measured at fair value.

6 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2.2.2 Lease payments

IFRS 16.27 A lessee includes the following payments relating to the use of the underlying

asset in the measurement of the lease liability:

– xed payments (including in-substance xed payments), less any lease

incentives receivable;

– variable lease payments that depend on an index or a rate;

– amounts expected to be payable by the lessee under residual value guarantees;

– the exercise price of a purchase option that the lessee is reasonably certain to

exercise; and

– payments for terminating the lease if the lease term reects early termination.

IFRS 16.B42 ‘In-substance xed payments’ are payments that are structured as variable lease

payments, but that – in substance – are unavoidable. Examples include:

– payments that have to be made only if an event occurs that has no genuine

possibility of not occurring;

– there is more than one set of payments that a lessee could make, but only one

of those sets of payments is realistic; and

– there are multiple sets of payments that a lessee could realistically make, but it

has to make at least one set of payments.

IFRS 16.27–28, BC166 Variable lease payments that depend on an index or rate are initially measured

using the index or rate as at the commencement date of the lease. Such payments

include payments linked to a consumer price index (CPI), payments linked to a

benchmark interest rate (such as IBOR) or payments that vary to reect changes in

market rental rates.

Variable lease payments that are highly probable to occur are not in-substance

xed payments if they are based on performance or use of the underlying asset

and are therefore avoidable.

IFRS 16.27(c), A If a lessee provides a residual value guarantee, then it includes in the lease

payments the amount that it expects to pay under that guarantee. An

unguaranteed residual value is always excluded from the determination of the

lease payments by the lessee.

IFRS 16.27, B37 Lessees determine whether it is reasonably certain that they will exercise a

purchase option considering all relevant facts and circumstances that create an

economic incentive to do so. This is similar to the approach for assessing whether

a lessee expects to exercise a renewal option (see Section 6.4).

Example 1 – In-substance xed payments: Minimum lease

payment

IFRS 16.27, 38(b), B42 Lessee W leases a production line from Lessor L. The lease payments depend

on the number of operating hours of the production line – i.e. W has to pay

1,000 per hour of use. The expected usage per year is 1,500 hours. If the usage

is less than 1,000 hours, then W must pay 1,000,000.

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Lessee accounting 7

2.2 Initial measurement of the lease liability

This lease contains in-substance xed payments of 1,000,000 per year, which

are included in the initial measurement of the lease liability. The additional

500,000 that W expects to pay per year are variable payments that depend on

usage and, therefore, are not included in the initial measurement of the lease

liability but are expensed as the ‘over-use’ occurs.

Example 2 – Variable payments not depending on an index or rate

IFRS 16.27 Utility Company C enters into a 20-year contract with Power CompanyD to

purchase electricity produced by a new solar farm. C and D assess that the

contract contains a lease. There are no minimum purchase requirements, and

no xed payments that C is required to make to D. However, C is required to

purchase all of the electricity produced by the solar plant at a priceof 10 per unit.

C notes that it is highly probable that the solar plant will generate at least some

electricity each year. However, the whole payment that C makes to D varies

with the amount of electricity produced by the solar farm – i.e. the payments

are fully variable. Therefore, C concludes that there are no in-substance xed

lease payments in this contract. C recognises the payments to D in prot or loss

when they are incurred.

Example 3 – Variable payments depending on an index

IFRS 16.28 Lessee Y rents an ofce building. The initial annual rental payment is 2,500,000.

Payments are made at the end of each year. The rent will be increased each year

by the change in the CPI over the preceding 12 months.

This is an example of a variable lease payment that depends on an index. The

initial measurement of the lease liability is based on the value of the CPI on

lease commencement – i.e. an annual rental of 2,500,000 for each year of the

lease. If during the rst year of the lease the CPI increases from 100 to 105 (i.e.

the rate of ination over the preceding 12 months is 5%), then at the end of

the rst year the lease liability is recalculated assuming future annual rentals of

2,625,000 (i.e. 2,500,000 × 105 / 100).

Example 4 – Residual value guarantees

IFRS 16.27(c) Lessee Z has entered into a lease contract with Lessor L to lease a car.The

lease term is ve years. In addition, Z and L agree on a residual value

guarantee– if the fair value of the car at the end of the lease term is below 400,

then Z will pay to L an amount equal to the difference between 400 and the fair

value of the car.

At commencement of the lease, if Z expects the fair value of the car at the end

of the lease term to be 380, then it includes 20 in the lease payments in respect

of the residual value guarantee when calculating the lease liability.

8 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Which variable lease payments are included in the initial

measurement of the lease liability?

IFRS 16.BC168–BC169 The initial measurement of the lease liability includes variable lease payments

that depend on an index or rate – e.g. the CPI or a market interest rate – and

payments that appear to be variable but are in-substance xed payments.

Variable lease payments that depend on sales or usage of the underlying asset

are excluded from the lease liability. Instead, these payments are recognised

in prot or loss in the period in which the performance or use occurs. This has a

number of importantconsequences.

– A lessee’s apparent indebtedness depends on the mix of xed and variable

payments within its lease portfolio. For example, suppose that Retailer X

leases a portfolio of retail outlets with xed lease payments. RetailerY leases

a similar portfolio of retail outlets on similar terms but with a mix of xed

lease payments and lease payments that depend on turnover. Xrecognises

higher lease liabilities than Y – even if the total expected lease payments for

Xand Y are the same.

– Some power purchase agreements that are leases may result in a lease

liability of zero for the lessee. For example, if a lessee enters into an

agreement to purchase all of the electricity produced by a wind farm or

hydroelectric plant and the lease payments all depend on the amount of

electricity produced, then the lessee’s lease liability is zero.

How does the lessee decide whether to include in the lease

liability amounts payable on exercise of a renewal, purchase or

termination option?

IFRS 16.18–19, 27(d)–(e), 70(d)–(e), A, B37–B40 The lessee determines whether it is reasonably certain to exercise an option

to extend the lease or to purchase the underlying asset, or not to exercise an

option to terminate the lease early. This assessment is made by considering all

relevant facts and circumstances that create an economic incentive to exercise

an option or not to do so (seeSection 6.4).

Each party determines the lease payments in a manner consistent with this

assessment as follows.

– Renewal option: If it is determined that the lessee is reasonably certain to

exercise a renewal option, then the lease payments include the relevant

payments for the period covered by the renewal option.

– Termination option: If it is determined that the lessee is not reasonably

certain not to terminate the lease early, then the lease payments include the

termination penalty.

– Purchase option: If it is determined that the lessee is reasonably certain to

exercise an option to purchase an underlying asset, then the lease payments

include the exercise price of the purchase option.

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Lessee accounting 9

2.2 Initial measurement of the lease liability

What are lease incentives and how are they accounted for by

lessees?

IFRS 16.A, 27(a) Lease incentives are payments made by a lessor to a lessee associated with a

lease, or the reimbursement or assumption by a lessor of the costs of a lessee.

Payments made by the lessor to the lessee are not lease incentives when they

are associated with other obligations of the lessee to transfer distinct goods or

services to the lessor.

Examples of lease incentives provided by lessors include up-front cash

payments to the lessee or assumption of costs of the lessee such as leasehold

improvements, relocation costs and costs associated with a pre-existing lease

commitment. Alternatively, initial periods of the lease term may be agreed to be

rent-free or at a reduced rent.

Irrespective of its form, a lease incentive is part of the lease payments – i.e. the

net consideration for the lease.

2.2.3 Discount rate

IFRS 16.26, A At the commencement date, a lessee measures the lease liability at the present

value of the lease payments using the interest rate implicit in the lease if this can

be readily determined. This is the rate that causes the present value of the lease

payments and the unguaranteed residual value to equal the sum of the fair value of

the underlying asset and any initial direct costs of the lessor.

If the lessee cannot readily determine the interest rate implicit in the lease, then

the lessee uses its incremental borrowing rate. This is the rate that a lessee

would have to pay at the commencement date of the lease for a loan of a similar

term, and with similar security, to obtain an asset of similar value to the right-of-

useasset in a similar economic environment.

10 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Is the rate implicit in the lease readily determinable for a lessee?

In most circumstances, a lessee is not able to determine the rate implicit in

the lease. There is no separate denition of the interest rate implicit in the

lease for the lessee. The lack of information available to the lessee (e.g. the

lessor’s initial direct costs, the initial fair value of the underlying asset and the

lessor’s expectations of the residual value of the asset at the end of the lease)

typically makes it difcult for the lessee to determine the interest rate implicit

in the lease. Therefore, it is likely to be difcult for lessees to readily determine

the interest rate implicit for most leases. As a result, lessees often use their

incremental borrowingrate.

Should a lessee’s incremental borrowing rate reect the interest

rate in a loan with both a similar maturity to the lease and a

similar payment prole to the lease payments?

IFRS 16.A, BC162, IU 09-19 In some cases, a lessee seeking to determine its incremental borrowing rate

may have readily observable evidence of the interest rate on a loan with the

same term but a different payment prole from the lease. A question arises

about whether a lessee’s incremental borrowing rate is required to reect the

interest rate in a loan with both a similar maturity to the lease and a similar

payment prole to the lease payments.

The IFRS Interpretations Committee discussed this matter and noted that

the denition of a lessee’s incremental borrowing rate requires the lessee to

determine its incremental borrowing rate for a particular lease considering the

terms and conditions of the lease. The Committee observed that it would be

consistent with the Board’s objective in developing the denition of incremental

borrowing rate for a lessee to refer as a starting point to a readily observable

rate for a loan with a similar payment prole to that of the lease, although IFRS

16 does not explicitly require this.

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Lessee accounting 11

2.3 Initial measurement of the right-of-use asset

2.3 Initial measurement of the right-of-use asset

IFRS 16.23–24 At the commencement date, a lessee measures the right-of-use asset at a cost

that includes the following.

IFRS 16.A A lessee’s ‘initial direct costs’ are the incremental costs of obtaining a lease that

would not otherwise have been incurred. This denition is similar to the denition

of the incremental costs of obtaining a contract under IFRS 15 Revenue from

Contracts with Customers. That is, the focus is on costs that are contingent on

actually obtaining the lease. Costs that are directly attributable to seeking to obtain

a lease but are incurred irrespective of whether the lease is actually obtained are

not initial direct costs.

12 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Typical initial direct costs of a lessee

Include

✔

Exclude

– Commissions

– Legal fees*

– Costs that are incremental and

directly attributable to negotiating

lease terms and conditions*

– Costs of arranging collateral

– Payments made by a potential

lessee to existing tenants to obtain

the lease

* If they are contingent on obtaining

thelease

– General overheads (e.g. costs

incurred by a sales and marketing

team or a purchase team)

– Costs of investment appraisals,

feasibility studies, due diligence

etc that are incurred regardless of

whether the lease is entered into

– Costs to obtain offers for potential

leases

2.4 Subsequent measurement of the lease

liability

2.4.1 Measurement basis

IFRS 16.36 After initial recognition, a lessee measures the lease liability by:

– increasing the carrying amount to reect interest on the lease liability;

– reducing the carrying amount to reect the lease payments made; and

– remeasuring the carrying amount to reect:

– any reassessment (see 2.4.2) or lease modications (see Section 7.2); and

– revised in-substance xed lease payments (see 2.4.2).

IFRS 16.37 Interest on the lease liability in each period during the lease term is the amount

that produces a constant periodic rate of interest on the remaining balance of

the lease liability. The ‘periodic rate of interest’ is the discount rate used in the

initial measurement of the lease liability (see2.2.3) or, if appropriate, the revised

discount rate (see 2.4.2 and Section 7.2).

IFRS 16.BC183 Lessees cannot choose to measure lease liabilities subsequently at fair value.

Example 5 – Lease liability: Subsequent measurement

Lessee X has entered into a contract with Lessor L to lease a building for

sevenyears. The annual lease payments are 450, payable at the end of each

year. X estimates that the incremental borrowing rate is 5.04% and uses it to

measure the lease liability. The initial recognition of the obligation to make lease

payments is 2,600.

X performs the following calculations at the end of Year 1.

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Lessee accounting 13

2.4 Subsequent measurement of the lease liability

Amount

Initial recognition of lease liability 2,600

Payment (450)

Repayment of interest (131)

(1)

Repayment of principal (319)

(2)

(319)

Carrying amount of liability at end of Year 1 2,281

(3)

Notes

1. Calculated as 2,600 × 5.04%.

2. Calculated as 450 - 131.

3. Calculated as 2,600 - 319.

2.4.2 Remeasurement of the lease liability

IFRS 16.39 After the commencement date, a lessee remeasures the lease liability to reect

changes in the lease payments. This occurs when the lessee reassesses whether

it is reasonably certain to exercise an option to extend the lease or to purchase

the underlying asset, or not to exercise an option to terminate the lease early. In

addition, the lessee revises the lease term and remeasures the lease liability when

there is a change in the non-cancellable period of a lease. See Section 6.6 for a

detailed discussion.

Thefollowing table describes which discount rate to use for the remeasurement.

IFRS 16.36(c), 40–43, B42(a)(ii)

14 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Example 6 – Lease liability: Change in variable payments linked to

an index

LesseeY enters into a lease for a ve-year term with Lessor L for a retail

building, commencing on 1 January.Y pays 155 per year, in arrears.Y’s

incremental borrowing rate is 5.9%. Additionally, the lease contract states

that lease payments for each year will increase on the basis of the increase in

the CPI for the preceding year. At the commencement date, the CPI for the

previous year is 120 and the lease liability is 655 based on annual payments of

155 discounted at 5.9% to the commencement date.

Assume that initial direct costs are zero and there are no lease incentives,

prepayments or restoration costs.Y records the following entries forYear 1.

Debit Credit

Right-of-use asset 655

Lease liability 655

To recognise lease at commencement date

Depreciation 131

Right-of-use asset 131

Interest expense (655 × 5.9%) 39

Lease liability (155 - 39) 116

Cash (payment forYear 1) 155

To recognise payment and expenses forYear 1

At the end ofYear 1, the CPI increases to 125.Y calculates the revised

payments forYear 2 and beyond adjusted for the change in CPI as 161 (155 ×

125 / 120). Because the lease payments are variable payments that depend on

an index, Y adjusts the lease liability to reect the change. The adjustment is

calculated as the difference between the original lease payments (155) and the

reassessed payment (161) over the remaining four-year lease term, discounted

at the original discount rate of 5.9% (21).

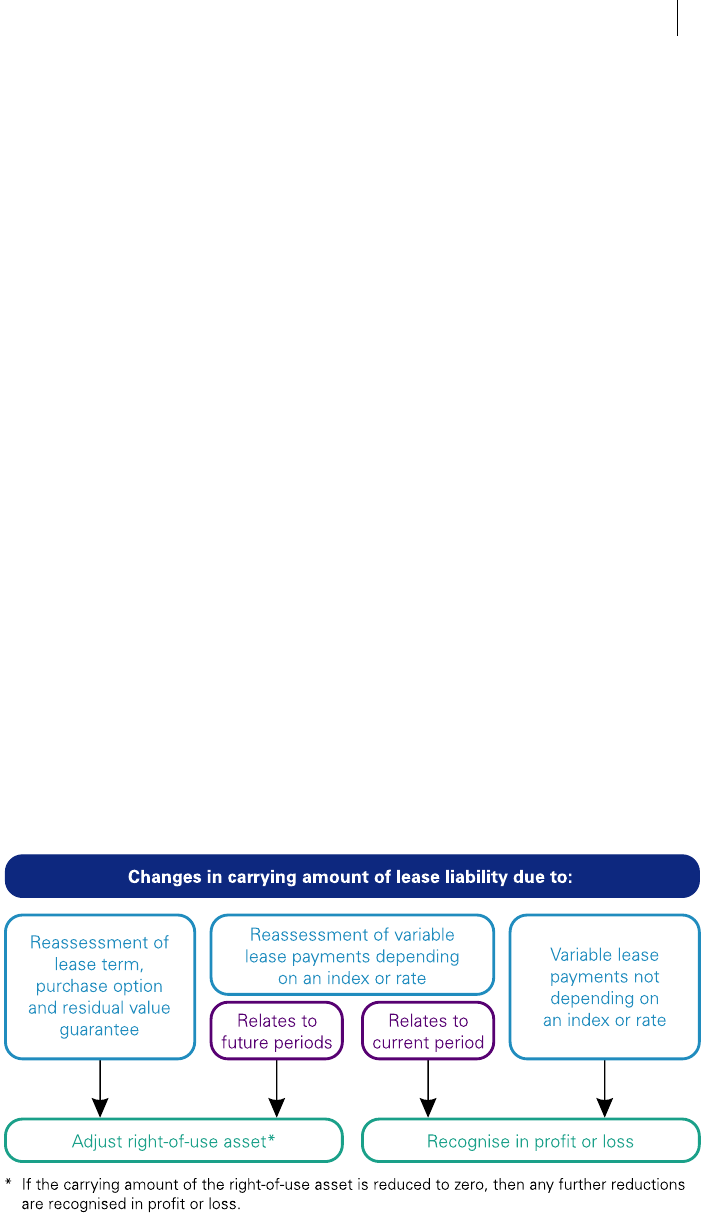

Remeasurements of variable lease payments that depend on an index and

relate to future periods are reected in the carrying amount of the right-of-use

asset (see Section 3.5). Y records the following entry.

Debit Credit

Right-of-use asset 21

Lease liability 21

To recognise remeasurement

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Lessee accounting 15

2.5 Subsequent measurement of the right-of-use asset

2.5 Subsequent measurement of the right-of-use

asset

2.5.1 Measurement basis

IFRS 16.29–30 Generally, a lessee measures right-of-use assets at cost less accumulated

depreciation (see 2.5.2) and accumulated impairment losses (see 2.5.3).

IFRS 16.30(b), 38(b), 39 The lessee adjusts the carrying amount of the right-of-use asset for the

remeasurement of the lease liability – e.g. when there is a change in CPI (see

2.4.2). If the carrying amount of the right-of-use asset has already been reduced to

zero and there is a further reduction in the measurement of the lease liability, then

the lessee recognises any remaining amount of the remeasurement in prot or

loss.

IFRS 16.34–35, IAS 40.2 A lessee applies alternative measurement bases in two circumstances:

– if the right-of-use asset meets the denition of investment property, then the

lessee measures the right-of-use asset in accordance with its accounting policy

for all of its investment property, which may be at fair value; and

– if a lessee applies the revaluation model to a class of property, plant and

equipment, then it may elect to apply the revaluation model to all right-of-use

assets that belong to the same class.

IFRS 16.38–39 The following diagram summarises the impact of changes in the carrying amount

of the lease liability on the right-of-use asset.

2.5.2 Depreciation of the right-of-use asset

IFRS 16.31, IAS 16.60 A lessee depreciates right-of-use assets in accordance with the requirements

of IAS16 Property, Plant and Equipment – i.e. the depreciation method reects

the pattern in which the future economic benets of the right-of-use asset are

consumed. This will usually result in a straight-line depreciation charge.

IFRS 16.32 Depreciation starts at the commencement date of the lease. The period over which

the asset is depreciated is determined as follows:

16 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

– if ownership of the underlying asset is transferred to the lessee, or the lessee

is reasonably certain to exercise a purchase option, then the depreciation period

runs to the end of the useful life of the underlying asset; otherwise

– the depreciation period runs to the earlier of the end of the useful life of the

right-of-use asset or the end of the lease term.

Example 7 – Right-of-use asset: Depreciation period

Lessee X enters into a non-cancellable, non-renewable ve-year lease with

Lessor L for a machine that will be used in X’s manufacturing process. The

useful life of the underlying machine is 10 years and ownership remains withL.

Ownership does not transfer to X; therefore, X depreciates the right-of-use

asset from the commencement date over a period of ve years (i.e. the end of

the leaseterm).

Does IAS 16 component accounting apply to depreciation of

leases?

IFRS 16.31, IAS 16.43 Yes. IFRS 16 states that a lessee applies the depreciation requirements in

IAS 16 and therefore identies separate components for the purposes of

depreciation. This can be an important practical consideration for lessees that

lease big-ticket items under operating leases and adopt a component approach

to maintenance accounting – e.g. major maintenance checks in some aircraft

leases.

2.5.3 Impairment of the right-of-use asset

IFRS 16.33, IAS 36.63 A lessee applies IAS 36 Impairment of Assets to determine whether a right-of-

use asset is impaired and to account for any impairment. After recognition of an

impairment loss, the future depreciation charges for the right-of-use asset are

adjusted to reect the revised carrying amount.

Example 8 – Impairment of the right-of-use asset

Lessee Y leases a machine for its manufacturing process over a non-cancellable

10-year period. The initial carrying amount of the right-of-use asset is 1,000,

which is subsequently measured at cost and depreciated on a straight-line basis

over a period of 10 years – i.e. the depreciation charge per year amounts to 100.

At the end of Year 5, the cash-generating unit that includes the right-of-use asset

is impaired. An impairment charge of 200 is allocated to the right-of-useasset.

Immediately before the impairment, the carrying amount of the right-of-use

asset is 500. Following the impairment, the carrying amount is reduced to 300

and the future depreciation charges are reduced to 60 (300 / 5) per year.

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Lessee accounting 17

2.6 Recognition exemptions for lessees

2.6 Recognition exemptions for lessees

IFRS 16.5, A A lessee can elect not to apply the lessee accounting model to:

– leases with a lease term of 12 months or less that do not contain a purchase

option: i.e. short-term leases (see 2.6.1); and

– leases for which the underlying asset is of low value when it is new: even if the

effect is material in aggregate (see 2.6.2).

IFRS 16.6 If a lessee elects to apply either of these recognition exemptions, then it

recognises the related lease payments as an expense on either a straight-line

basis over the lease term, or another systematic basis if that basis is more

representative of the pattern of the lessee’s benet.

2.6.1 Short-term leases

IFRS 16.8 The election for short-term leases is made by class of underlying asset. A ‘class

of underlying asset’ is a grouping of underlying assets of a similar nature and use

in the lessee’s operations. When electing the short-term lease exemption for a

particular class of underlying asset, only underlying assets from leases that meet

the denition of a short-term lease are considered.

IFRS 16.A The ‘lease term’ is determined in a manner consistent with that for all other leases

(see Chapter 6). Consequently, the short-term lease exemption may be applied

to renewable and cancellable leases (e.g. month-to-month, evergreen leases)

if the lessee is not reasonably certain to renew (or to continue, in the case of a

termination option) the lease beyond 12 months.

Example 9 – Recognition exemption: Short-term lease

IFRS 16.18, B34–B35, B37

Lessee L manufactures toys. L enters into a 10-year lease of a non-specialised

machine to be used in manufacturing parts for Racing Car X1. It expects this

model of toy to remain popular with customers until it completes development

and testing of an improved model – Racing Car X2. The current machine can

be easily replaced and the cost to install it in L’s manufacturing facility is not

signicant. L, but not the lessor, has the right to terminate the lease without

penalty on each anniversary of the lease commencement date.

18 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

The non-cancellable period is one year (see Section 6.2). In addition, because

the machine is not specialised, it can easily be replaced and the cost to install

the machine in L’s manufacturing facility is not signicant. L determines that it is

not reasonably certain to continue the lease after the rst year (see Section 6.4).

As a result, the lease term is also one year and the lease qualies for the short-

term leaseexemption.

What happens if the lessee applies the short-term lease exemption

and there are changes in the lease term?

IFRS 16.7 If a lessee elects to apply the short-term lease recognition exemption and there

are any changes to the lease term – e.g. the lessee exercises an option that it

had previously determined that it was not reasonably certain to exercise – or the

lease is modied, then the lessee accounts for the lease as a new lease.

2.6.2 Low-value items

IFRS 16.5(b), 8, B3–B8 A lessee is permitted not to apply the recognition and measurement requirements

to leases of assets that, when they are new, are of low value. This exemption,

unlike the short-term lease exemption, can be applied on a lease-by-lease basis.

IFRS 16.B5 A lessee does not apply the low-value exemption to a lease of an individual asset

in either of the following scenarios:

– if the underlying asset is highly dependent on, or highly inter-related with, other

assets; or

– if the lessee cannot benet from the underlying asset on its own or together

with other readily available resources, irrespective of the value of that

underlying asset.

IFRS 16.B7 The low-value exemption also does not apply to a head lease for an asset that is

sub-leased or that is expected to be sub-leased. When a lessee neither enters

into a sub-lease immediately nor expects to do so later, it may elect to apply

theexemption.

IFRS 16.B6, B8, BC98–BC104 IFRS 16 does not specify a threshold for the low-value exemption, but the

basis for conclusions states that the Board ‘had in mind’ assets with a value of

approximately USD 5,000 or less when they are new, such as small IT equipment

(e.g. some laptops, desktops, tablets, mobile phones, individual printers) and

some ofce furniture – i.e. ‘inexpensive’ assets. The exemption is not intended to

capture underlying assets such as cars and most photocopiers.

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Lessee accounting 19

2.6 Recognition exemptions for lessees

Example 10 – Recognition exemption: Low-value items

IFRS 16.IE3 Lessee B is in the pharmaceutical manufacturing and distribution industry and

leases the following:

– real estate, both ofce building and warehouse;

– inexpensive ofce furniture;

– company cars, both for sales personnel and for senior management and of

varying quality, specication and value;

– trucks and vans used for delivery; and

– inexpensive IT equipment – e.g. laptops.

B determines that the leases of inexpensive ofce furniture and laptops qualify

for the recognition exemption on the basis that the underlying assets, when

they are new, are individually of low value. Although the low-value exemption

can be applied on a lease-by-lease basis, B elects to apply the exemption to

all of these leases. In contrast, B applies the recognition and measurement

requirements of IFRS16 to its leases of real estate, company cars, trucks

andvans.

What happens if the exemption is applied and the underlying asset

is subsequently sub-leased?

IFRS 16.7, B7 If a lessee sub-leases, or expects to sub-lease, an asset, then the head lease

does not qualify as a lease of a low-value item. When a lessee neither enters

into a sub-lease immediately nor expects to do so later, it may elect to apply

theexemption.

However, if a lessee initially elects to use the low-value exemption – because

it expects not to sub-lease the asset – but subsequently does enter into a sub-

lease, then the lease would no longer qualify for the exemption. It appears that

at the date of the change, the lessee should consider the lease to be a new

lease. In these cases, the lessee also considers whether the reason for the

change in intention provides evidence about whether other leases of low-value

items do or do not qualify for the exemption.

20 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2.7 Presentation and disclosure

2.7.1 Lessee presentation

IFRS 16.47–50 A lessee presents leases in its nancial statements as follows.

Statement of nancial

position

Statement of prot

or loss and other

comprehensive income

Statement of cash

ows

Right-of-use asset

– Separate presentation

in the statement of

nancial position*

or disclosure in the

notes to the nancial

statements

Lease liability

– Separate presentation

in the statement of

nancial position or

disclosure in the notes

Lease expenses

– Separate presentation

of interest expense on

the lease liability from

depreciation of the

right-of-use asset

– Presentation of

interest expense

as a component of

nancecosts

Operating activities

– Variable lease

payments not included

in the leaseliability

– Payments for short-

term and low-value

leases (subject to

use of recognition

exemption)

Financing activities

– Cash payments for

principal portion of

lease liability

Depending on

‘general’ allocation

– Cash payments for

the interest portion

are classied in

accordance with other

interest paid

* Right-of-use assets that meet the denition of investment property are presented within

investment property.

2.7.2 Lessee disclosure

IFRS 16.51 A lessee discloses information that provides a basis for users of nancial

statements to assess the effect that leases have on nancial position, nancial

performance and cash ows.

IFRS 16.52 A lessee discloses information about leases for which it is a lessee in a single

note or separate section in the nancial statements. However, a lessee does not

need to duplicate information that is already presented elsewhere in the nancial

statements, provided that the information is incorporated by cross-reference in the

single note or separate section about leases.

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Lessee accounting 21

2.7 Presentation and disclosure

IFRS 16.53–60, IAS 16.77 Extensive disclosures are required by lessees. These are addressed in our Guides

to nancial statements.

Normally, a lessee discloses at least the following information.

Quantitative information

IFRS 16.47, 53, 58

Relating to the statement of nancial position

– Additions to right-of-use assets

– Year-end carrying amount of right-of-use assets by class of underlying asset

and (if they are not presented separately) the corresponding line items in the

statement of nancial position

– Lease liabilities and the corresponding line items in the statement of nancial

position if lease liabilities are not presented separately

– Maturity analysis for lease liabilities

IFRS 16.53–54

Relating to the statement of prot or loss and other comprehensive

income (including amounts capitalised as part of the cost of another

asset)

– Depreciation charge for right-of-use assets by class of underlying asset

– Interest expense on lease liabilities

– Expense relating to short-term leases for which the recognition exemption is

applied (leases with a lease term of up to one month can be excluded)

– Expense relating to leases of low-value items for which the recognition

exemption is applied

– Expense relating to variable lease payments not included in lease liabilities

– Income from sub-leasing right-of-use assets

– Gains or losses arising from sale-and-leaseback transactions

IFRS 16.53

Relating to the statement of cash ows

– Total cash outow for leases

IFRS 16.55

Other

– Amount of short-term lease commitments if current short-term lease expense

is not representative for the following year

Qualitative disclosures

IFRS 16.58, 60, 7.B11 – Description of how liquidity risk related to lease liabilities is managed

– Use of exemption for short-term and/or low-value item leases

22 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Additional disclosures (when applicable)

IFRS 16.56–57, IAS 16.77 – Disclosures required by IAS 40 Investment Property for right-of-use assets

qualifying as investment property

– If the revaluation model of IAS 16 is applied for right-of-use assets, then:

- Effective date of revaluation

- Whether an independent valuer was involved

- Carrying amount that would have been recognised under the cost model

- Revaluation surplus, change for the period and any distribution restrictions

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3 Lessor accounting 23

3.1 Lessor accounting model

3 Lessor accounting

Lessors continue to classify leases as nance or operating leases.

3.1 Lessor accounting model

IFRS 16.B53, BC289 The lessor follows a dual accounting approach for lease accounting. The accounting

is based on whether signicant risks and rewards incidental to ownership of an

underlying asset are transferred to the lessee, in which case the lease is classied

as a nance lease. This is similar to the previous lease accounting requirements

that applied to lessors. The lessor accounting models are also essentially

unchanged from IAS 17 Leases.

Are the lessee and lessor accounting models consistent?

No. A key consequence of the decision to retain the IAS 17 dual accounting

model for lessors is a lack of consistency with the new lessee accounting

model. This can be seen in Example 11 below:

– the lessee applies the right-of-use model and recognises a right-of-use asset

and a liability for its obligation to make lease payments; whereas

– the lessor continues to recognise the underlying asset and does not

recognise a nancial asset for its right to receive lease payments.

There are also more detailed differences. For example, lessees and lessors

use the same guidance for determining the lease term and assessing whether

renewal and purchase options are reasonably certain to be exercised, and

termination options not reasonably certain to be exercised. However, unlike

lessees, lessors do not reassess their initial assessments of lease term and

whether renewal and purchase options are reasonably certain to be exercised,

and termination options not reasonably certain to be exercised (see Section

6.6).

Other differences are more subtle. For example, although the denition of lease

payments is similar for lessors and lessees (see 2.2.2), the difference is the

amount of residual value guarantee included in the lease payments.

– The lessor includes the full amount (regardless of the likelihood that payment

will be due) of any residual value guarantees provided to the lessor by the

lessee, a party related to the lessee or a third party unrelated to the lessor

that is nancially capable of discharging the obligations under the guarantee.

– The lessee includes only any amounts expected to be payable to the lessor

under a residual value guarantee.

24 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Are the IFRS 16 requirements for lessors identical to IAS 17?

No. The overall accounting models are essentially unchanged. However, there

are a number of changes in the details of lessor accounting. For example,

lessors apply the new:

– denition of a lease (see Chapter 4);

– sub-lease guidance (see Chapter 8);

– sale-and-leaseback guidance (see Chapter 9); and

– disclosure requirements (see Section 3.5).

In addition, IFRS 16 includes specic guidance on accounting for lease

modications by lessors (see Section 7.3).

3.2 Lease classication

IFRS 16.61–62, B53 A lessor classies a lease as either a nance lease or an operating lease,

asfollows:

– leases that transfer substantially all of the risks and rewards incidental to

ownership of the underlying asset are nance leases; and

– all other leases are operating leases.

The lease classication test is essentially unchanged from IAS 17.

IFRS 16.63 Generally, the presence of the following indicators, either individually or in

combination, leads to a lease being classied as a nance lease:

– transfer of ownership to the lessee either during or at the end of the lease term;

– existence of a purchase option that is reasonably certain to be exercised;

– the lease term is for a major part of the economic life of the underlying asset;

– the present value of the lease payments amounts to substantially all of the fair

value of the underlying asset at inception of the lease; and

– the underlying asset is specialised.

IFRS 16.66 Lease classication is made at the inception date and is reassessed only if there

is a lease modication. Changes in estimates (e.g. changes in estimates of the

economic life or of the residual value of the underlying asset), or changes in

circumstances (e.g. default by the lessee), do not give rise to a new classication

of a lease for accounting purposes.

IFRS 16.B54 However, if the contract includes terms and conditions to adjust the lease

payments for particular changes occurring between the inception date and the

commencement date, then, for the purpose of classifying the lease, the effect of

any such changes is deemed to have taken place at the inception date.

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3 Lessor accounting 25

3.2 Lease classication

Example 11 – Lease classication

Lessor L enters into a non-cancellable lease contract with Company X under

which X leases non-specialised equipment for ve years. The economic life of

the equipment is estimated to be 15 years and legal title will remain with L.

The lease contract contains no purchase, renewal or early termination options.

The fair value of the equipment is 100,000 and the present value of the lease

payments amounts to 50,000.

In assessing the classication of the lease, L notes that:

– the lease does not transfer ownership of the equipment to X;

– X has no option to purchase the equipment;

– the lease term is for one-third of the economic life of the equipment, which is

less than the major part of the economic life;

– the present value of the lease payments amounts to 50% of the fair value of

the equipment, which is less than substantially all of the fair value; and

– the equipment is not specialised.

L notes that there are no indicators that the lease is a nance lease and that,

based on an overall evaluation of the arrangement, the lease does not transfer

substantially all of the risks and rewards incidental to the ownership of the

equipment to X.

Therefore, L classies the lease as an operating lease.

Are there special rules on the classication of leases of land?

IFRS 16.B55, BCZ241–BCZ244 No. The classication of a lease of land is assessed based on the general

classication guidance. An important consideration is that land normally has

an indenite economic life. However, the fact that the lease term is normally

shorter than the economic life of the land does not necessarily mean that a

lease of land is always an operating lease; the other classication requirements

are also considered.

For example, in a 99-year lease of land with xed lease payments, the signicant

risks and rewards associated with the land are transferred to the lessee during

the lease term, and on lease commencement the present value of the residual

value of the land would be negligible. It follows that a long lease term may

indicate that a lease of land is a nance lease.

There is no bright-line threshold for the lease term above which a lease of land

would always be classied as a nance lease, and assessing classication can

require the use of signicant judgement in some cases.

26 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Do changes between the inception and commencement dates

impact lease classication?

IFRS 16.66–67, 70–71, B54 Yes, in some cases. Generally, the classication of a lease is determined

at inception of thelease and is not revised unless the lease agreement is

modied. However, the classication is updated for certain changes between

inception date and commencement date that are deemed to have taken place at

the inception date.

A signicant amount of time may pass between the inception date and the

commencement date – e.g. when parties commit to leasing an underlying

asset that has not yet been built. A lease contract may also include terms and

conditions to adjust the lease payments for changes that occur between the

inception date and the commencement date – e.g. a change in the lessor’s cost

of the underlying asset or a change in the lessor’s cost of nancing the lease.

In such cases, the calculation of the present value of lease payments used in

determining the classication of the lease covers all lease payments made

from the commencement of the lease term. However, if the lease payments

are adjusted for contractual changes such as changes in the construction or

acquisition cost of the underlying asset, general price levels or the lessor’s

costs of nancing the lease between the inception and commencement dates,

then the effect of these changes is deemed to have taken place at inception for

the purpose of classifying the lease.

It appears that the lease payments for classication purposes should also be

updated for changes between the inception and commencement dates in:

– the non-cancellable period of the lease (see Section 6.2);

– lease payments that depend on an index or a rate; and

– variable payments that become in-substance xed.

We believe that these changes are akin to contractual changes between

the inception and commencement dates, and therefore the effect of these

changes should be deemed to have taken place at inception for the purpose of

classifying the lease. Consequently, a lessor should also update the rate implicit

in the lease and its estimate of the unguaranteed residual value for classication

purposes for such contractual changes.

However, for measurement purposes it appears that a lessor should update the

lease payments, the rate implicit in the lease and the unguaranteed residual value

for all changes between inception and commencement date. This is because

a lessor measures the net investment in a nance lease, and the amount of

operating lease income to be recognised, at the commencement date.

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3 Lessor accounting 27

3.3 Operating lease model

3.3 Operating lease model

The lessor classies a lease that is not a nance lease as an operating lease.

IFRS 16.81 If, before lease commencement, a lessor recognises an asset in its statement of

nancial position and leases that asset to a lessee under an operating lease, then

the lessor does not derecognise the asset on lease commencement. Generally,

future contractual rental payments from the lessee are recognised as receivables

over the lease term as the payments become receivable.

IFRS 16.81, 83 Generally, lease income from operating leases is recognised by the lessor on a

straight-line basis from the commencement date over the lease term. It may be

possible for the lessor to recognise lease income using another systematic basis

if that is more representative of the time pattern in which the benet from the use

of the underlying asset is diminished. Similarly, increases (or decreases) in rental

payments over a period of time, other than variable lease payments, are reected

in the determination of the lease income, which is recognised on a straight-line

basis.

IFRS 16.83 The initial direct costs incurred by the lessor in arranging an operating lease are

added to the carrying amount of the underlying asset and cannot be recognised

immediately as an expense. These initial direct costs are recognised as an expense

on the same basis as the lease income. This will not necessarily be consistent with

the basis on which the underlying asset is depreciated.

IFRS 16.81, A Incentives granted to the lessee in negotiating a new or renewed operating lease

are recognised as an integral part of the lease payments relating to the use of the

underlying asset. They are recognised as a reduction of rental income over the

lease term using the same recognition basis as for the lease income.

IFRS 16.84 The lessor depreciates the underlying asset over the asset’s useful life in a manner

that is consistent with the depreciation policy that it applies to similar owned

assets.

IFRS 16.85, 9.2.1(b)(i) A lessor applies IAS 36 to determine whether an underlying asset subject to an

operating lease is impaired and to account for any impairment loss identied.

In

addition, the lessor applies the impairment and derecognition requirements of

IFRS 9 to operating lease receivables.

Should a lessor continue to recognise operating lease income

on a straight-line basis if the lessee reduces actual usage of the

underlying asset?

IFRS 16.81

Generally, yes.

In most leases, the benet conveyed by the lessor to the lessee is the right to

use the underlying asset over the lease term. For this reason, operating lease

income from leases is typically recognised by the lessor on a straight-line basis

from the commencement date over the lease term.

28 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

IFRS 16 states that it is possible to recognise operating lease income using

another systematic basis if that is more representative of the time pattern in

which the benet of the underlying property is diminished. However, it is rare

that a basis other than straight-line meets this test in a lease. For example, in a

real estate lease, a retailer that leases a retail store from a landlord may expect

its sales at the store to vary seasonally, and may project year-on-year increases

in sales. However, the benet that the retailer receives under the lease is

the right to use the store. Therefore, if the lease payments are xed then the

landlord would recognise operating lease income on a straight-line basis in this

fact pattern.

A question arises about whether this approach remains appropriate if the

tenant signicantly reduces sales at the store and/or the government imposes

restrictions that reduce footfall at the store.

In the absence of a change in the lease agreement, the tenant’s benet under

the lease agreement remains the right to use the store. As long as the landlord

continues to convey the right to use the store to the retailer, the landlord will

typically continue to recognise operating lease income on a straight-line basis.

3.4 Finance lease model

IFRS 16.67–69, A At commencement, the lessor derecognises the underlying asset and recognises

a nance lease receivable at an amount equal to its net investment in the lease,

which comprises the present value of the lease payments and any

unguaranteed

residual value accruing to the lessor. The present value is calculated by discounting

the lease payments and any unguaranteed residual value, at the interest rate

implicit in the lease (see 2.2.3). Initial direct costs are included in the measurement

of the nance lease receivable, because the interest rate implicit in the lease takes

initial direct costs incurred into consideration.

IFRS 16.70(a) The lessor deducts any lease incentive payable from the lease payments included

in the measurement of the net investment in the lease.

The lessor recognises the difference between the carrying amount of the

underlying asset and the nance lease receivable in prot or loss when recognising

the nance lease receivable. This gain or loss is presented in prot or loss in the

same line item as that in which the lessor presents gains or losses from sales of

similar assets.

IFRS 16.75–76 Over the lease term, the lessor accrues interest income on the net investment.

The receipts under the lease are allocated between reducing the net investment

and recognising nance income, to produce a constant rate of return on the net

investment.

IFRS 16.77 A lessor applies the derecognition and impairment requirements of IFRS 9 to

the net investment in the lease. A lessor recognises any loss allowance on the

nance lease receivable, applying IFRS 9. A lessor regularly reviews estimated

unguaranteed residual values used in computing the gross investment in the

lease. If there is a reduction in the estimated unguaranteed residual value, then

the lessor revises the income allocation over the lease term without changing the

discount rate and immediately recognises any reduction in respect of amounts

accrued. For a discussion on measuring the expected credit losses on lease

receivables, see Chapter 7.8 in the 17th Edition 2020/21 of our publication Insights

into IFRS.

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3 Lessor accounting 29

3.5 Presentation and disclosure

3.5 Presentation and disclosure

3.5.1 Lessor presentation

A lessor presents leases in its statement of nancial position as follows.

Finance lease Operating lease

Statement of nancial position

IFRS 16.67, 88

– Present assets held under a nance

lease as a receivable at an amount

equal to the net investment in the

lease

– Present the underlying assets

subject to operating leases

according to the nature of the

underlying asset

3.5.2 Lessor disclosure

IFRS 16.89 A lessor discloses information that provides a basis for users of nancial statements

to assess the effect that leases have on nancial position, nancial performance and

cash ows. Extensive disclosures are required by lessors for nance and operating

leases. These are addressed in our Guides to nancial statements.

Normally, a lessor discloses at least the following information.

Finance lease Operating lease

Quantitative information

IFRS 16.90, 93–97

– Selling prot or loss

– Finance income on the net

investment in the lease

– Lease income relating to variable

lease payments not included in the

net investment in the lease

– Lease income relating to variable

lease payments that do not depend

on an index or rate

– Other lease income

– Detailed maturity analysis of the

undiscounted lease payments to

be received on an annual basis for

a minimum of each of the rst ve

years and a total of the amounts for

the remaining years

– Signicant changes in the carrying

amount of the net investment in

thelease

– Detailed maturity analysis of the

lease payments receivable

– A reconciliation between the

undiscounted lease payments

and the net investment in the

lease, identifying the unearned

nance income and any discounted

unguaranteed residual value

– If applicable, disclosures in

accordance with IAS 16 (separately

from other assets), IAS 36, IAS 38

Intangible Assets, IAS40 and IAS 41

Agriculture

30 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Finance lease Operating lease

Qualitative information

IFRS 16.93

– Signicant changes in the carrying

amount of the net investment in

thelease

– N/A

IFRS 16.92 A lessor also discloses quantitative and qualitative information about its leasing

activities, such as:

– the nature of its leasing activities; and

– how it manages risks associated with rights that it retains in underlying assets.

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

4 Lease denition 31

4.1 Overview

4 Leasedefinition

Lease denition is a key area of judgement in applying the

standard – a de facto on/off-balance sheet test for lessees.

4.1 Overview

IFRS 16.9, A A contract is, or contains, a lease if it conveys the right to control the use of

an identied asset (the underlying asset) for a period of time in exchange for

consideration.

The key elements of the denition are therefore as follows.

However, a lessee is not required to apply the lessee accounting model to leases

that qualify for certain practical expedients (see Section 2.6).

32 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

4.2 Identied asset

IFRS 16.B13–B20 A contract contains a lease only if it relates to an identied asset.

4.2.1 Specied asset

IFRS 16.B13, BC111 An asset can be either explicitly specied in a contract (e.g. by a serial number or

a specied oor of a building) or implicitly specied at the time it is made available

for use by the customer.

What does ‘implicitly specied’ mean?

An asset is implicitly specied if the facts and circumstances indicate that the

supplier can full its obligations only by using a specic asset. This may be the

case if the supplier has only one asset that can full the contract. For example,

a power plant may be an implicitly specied asset in a power purchase contract

if the customer’s facility is in a remote location with no access to the grid, such

that the supplier cannot buy the required energy in the market or generate it

from an alternative power plant.

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

4 Lease denition 33

4.2 Identied asset

In other cases, an asset may be implicitly specied if the supplier owns a

number of assets with the required functionality, but only one of those assets

can realistically be supplied to the customer within the contracted timeframe–

i.e. the supplier does not have a substantive right to substitute an alternative

asset to full the contract – see 4.2.3. For example, a supplier may own a eet

of vessels but only one vessel that is in the required geographic area and not

already being used by other customers.

4.2.2 Capacity portions

IFRS 16.B20 A capacity portion of an asset can be an identied asset if:

– it is physically distinct (e.g. a oor of a building, a specied strand of a bre-

optic cable or a distinct segment of a pipeline); or

– it is not physically distinct, but the customer has the right to receive

substantially all of the capacity of the asset (e.g. a capacity portion of a bre-

optic cable that is not physically distinct but represents substantially all of the

capacity of the cable).

Example 12 – Identied asset: Capacity portion is not an identied

asset

Customer D enters into an arrangement with Supplier E for the right to

store its gas in E’s specied storage tank. The storage tank has no separate

compartments. At inception of the contract, D has the right to use up to 60% of

the capacity of the storage tank throughout the term of the contract. E can use

the other 40% of the storage tank as it seest.

E has no substitution rights. However, the arrangement allows E to store gas

from other customers in the same storage tank.

In this scenario, there is no identied asset. This is because D only has rights

to 60% of the storage tank’s capacity and that capacity portion is not physically

distinct – i.e. is not physically separated – from the remainder of the tank, and

does not represent substantially all of the capacity of the storage tank.

34 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Example 13 – Identied asset: Capacity portion is an identied

asset

Customer C enters into an arrangement with Supplier S for the right to store

its products in a specied storage warehouse. Within this storage warehouse,

rooms V, W and X are contractually allocated to C for its exclusive use. S has no

substitution rights. Rooms V, W and X represent 60% of the warehouse’s total

storage capacity.

In this example, there is an identied asset. This is because:

– the rooms are explicitly specied in the contract;

– the rooms are physically distinct from the other storage locations within the

warehouse; and

– S has no (substantive) substitution rights.

Does ‘substantially all’ of the capacity of an asset mean

90percent?

Not necessarily. IFRS 16 does not dene what is meant by ‘substantially all’ in

the context of the denition of a lease.

IFRS 16 uses the same phrase in one of the criteria used by the lessor to

determine lease classication: whether the present value of the lease

payments (including the residual value guaranteed by the lessee or a third party)

equals or exceeds substantially all of the fair value of the asset. USGAAP allows

but does not require the use of a threshold of 90 percent for ‘substantially all’

when a lessor is determining classication. In our view, although the 90 percent

threshold may provide a useful reference point, it does not represent a bright-

line or automatic cut-off point under IFRS Standards.

For the purpose of applying the lease denition, a company should develop an

interpretation of ‘substantially all’ and apply it on a consistent basis.

4.2.3 Substantive supplier substitution rights

IFRS 16.B14 Even if an asset is specied in a contract, a customer does not control the use of

an identied asset if the supplier has a substantive right to substitute the asset for

an alternative asset. Such a right exists if the supplier:

– has the practical ability to substitute the asset throughout the period of use; and

– would benet economically from exercising its right to substitute the asset.

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

4 Lease denition 35

4.2 Identied asset

IFRS 16.B18

A supplier’s right or obligation to substitute the asset for repairs and maintenance,

because the asset is not working properly – i.e. a ‘warranty-type’ obligation–

or because a technical upgrade becomes available, is not a substantive

substitutionright.

IFRS 16.B14(a) A supplier has the practical ability to substitute alternative assets when the

customer cannot prevent it from substituting the asset and the supplier has

alternative assets either readily available or available within a reasonable period

oftime.

IFRS 16.B15 However, there is no practical ability to substitute the asset throughout the period

of use (and therefore there is no substantive substitution right) if the substitution

right applies, for example, only:

– to a part of the period of use or at or after a specic date; or

– on the occurrence of a particular event.

IFRS 16.A The ‘period of use’ is the total period of time that an asset is used to full a

contract with a customer (including any non-consecutive periods of time).

IFRS 16.B14(b) A supplier would benet economically from the exercise of its right to substitute

the asset when the economic benets associated with substituting the asset are

expected to exceed the related costs.

IFRS 16.B17 The costs associated with substitution are generally higher if the asset is not

located at the supplier’s premises – i.e. when it is at the customer’s premises

or elsewhere. In this situation, the costs are more likely to exceed the benets

associated with substituting the asset.

Example 14 – Identied asset: Substantive substitution right

Customer L enters into a ve-year contract with Freight Carrier M for the use of

rail cars from M to transport a specied quantity of goods. M uses rail cars of a

particular specication, and has a large pool of similar rail cars that can be used

to full the requirements of the contract. The rail cars and engines are stored

at M’s premises when they are not being used to transport goods. The costs

associated with substituting the rail cars are minimal for M.

Relevant experience demonstrates that:

– M benets economically from being able to deploy alternative assets as

necessary to full its contracts with customers; and

– the conditions that make substitution economically benecial are likely to

continue throughout the period of use.

In this case, because the rail cars are stored at M’s premises, it has a large pool

of similar rail cars and substitution costs are minimal, M has the practical ability

to substitute the assets – i.e. the rail cars are not implicitly specied. In addition,

the substitution is economically benecial to M throughout the period of use.

Therefore, M’s substitution rights are substantive and the arrangement does

not contain a lease.

36 | IFRS 16 – An overview: The new normal for lease accounting

© 2021 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Example 15 – Identied asset: No substantive substitution right

Customer L enters into an eight-year contract with Supplier K that requires K to