2023 Annual Report

CRH creates solutions that solve today’s

challenges to make a better tomorrow.

As the leading provider of building materials

solutions that build, connect and improve our

world, CRH helps to make construction easier,

safer and more sustainable.

We are the essential partner for transportation

and critical utility infrastructure projects,

complex non-residential construction and

outdoor living solutions.

The future imagined.

The future made.

2023 Performance Highlights

Strong delivery and further growth

across all key metrics

* Represents a non-GAAP measure. See the 'Non-GAAP Reconciliation' on pages xi to xiii.

1

Operating cash flow refers to net cash provided by operating activities as reported in the Consolidated Statements of Cash Flows.

2021 2022 2023

Revenues

$34.9bn

+7% p

2021 2022 2023

Adjusted EBITDA*

$6.2bn

+15% p

2021 2022 2023

Adjusted EBITDA Margin*

17.7%

+120bps p

2021 2022 2023

Operating Cash Flow

1

$5.0bn

+32% p

2021 2022 2023

Return on Net Assets

(RONA)*

15.3%

+200bps p

2021 2022 2023

Earnings Per Share (EPS)

Pre-impairment*

$4.65

+30% p

$32.7bn

$34.9bn

$5.4bn

$6.2bn

$29.2bn $4.8bn

16.5%

17.7%

16.5%

$3.8bn

$5.0bn $4.0bn

13.3%

15.3%

12.7%

$3.58

$4.65

$3.12

Leading the transition to smarter, sustainable construction to help reinvent the way our world is built

Overview of our business

CRH reimagines and reinvents new ways to build, connect and improve our world. Employing approximately 78,500 people at 3,390 operating locations in

29 countries, CRH has market leadership positions in both North America and Europe. Ranked among sector leaders by Environmental, Social and

Governance (ESG) rating agencies, CRH’s building materials solutions play an important role in shaping a more sustainable built environment.

1,2,3

Geographic Positioning

North America Sales by Region Europe Sales by Region

4

Annual Report 2023 ii

2

End-market exposures are approximate and derived from management estimates.

1

3

Market leadership positions are based on annualized sales volumes. This includes volumes which are used internally (e.g. aggregates supplied internally for cement production).

2

4

For the purposes of this overview, revenues from Asia-Pacific have been aggregated into Europe.

3

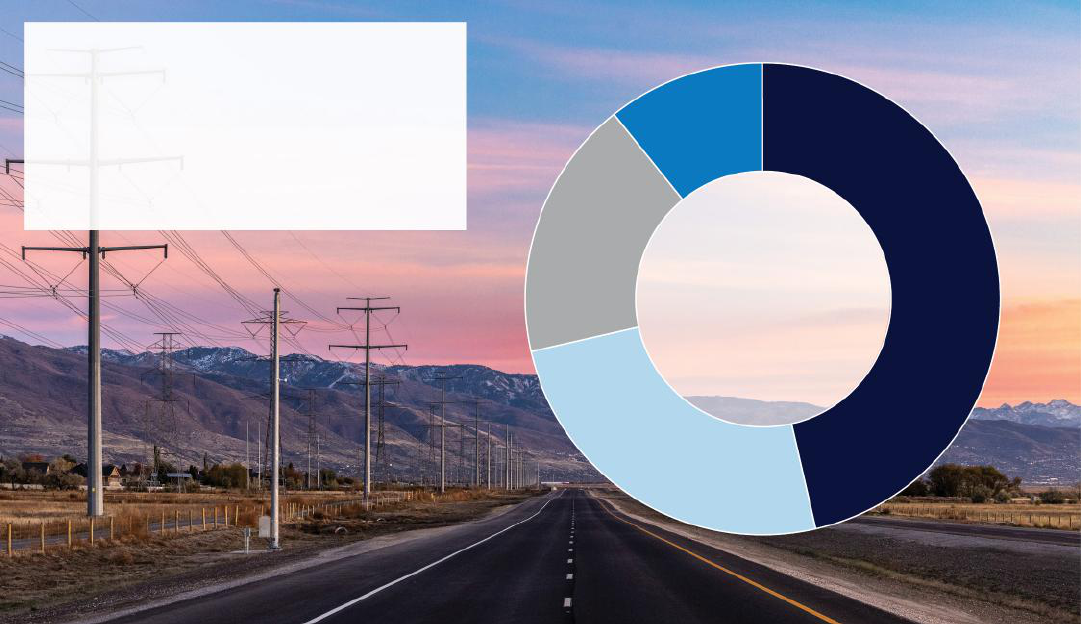

Sales by Division

65%

35%

Americas

Europe

Sales by End-Market

35%

30%

35%

Infrastructure

Non-Residential

Residential

Leadership Positions

3

#1 Aggregates - North America

#1 Asphalt - North America

#1 Concrete Products - North America and Europe

#3 Readymixed Concrete - North America

#3 Cement - North America and Europe

2

45%

30%

25%

South

North

West

65%

35%

Western Europe

Central and Eastern Europe

20%

45%

35%

CRH 2023 10-K Draft

v

Annual Report 2023

iii

A customer-centric approach

Developing new technologies

• Always striving to improve construction

design, installation & efficiency

Investing in Innovation

• Collaborating with customers to deliver a

higher performing built environment

Leveraging our scale and expertise

• Materials science

• Design concepts

• Technical expertise

• Manufacturing capabilities

Uniquely integrating

• Materials, products & services across the

construction value chain

Essential Materials

Aggregates

Cement

Products and Services

Readymixed Concrete

Asphalt

Infrastructural Concrete

Paving & Construction Services

Infrastructure Products

Architectural Products

Roads Solutions Utility Infrastructure Solutions Outdoor Living Solutions

Complete end-to-end solutions for our customers

Examples of our fully integrated solutions strategy in action

CRH’s differentiated strategy captures value across the supply chain, optimizing profits, cash and returns

for shareholders

We don't supply, we solve.

We transform Essential Materials (aggregates and cement) ...

• Finite, valuable & difficult to replace

• Key component in production of readymixed

concrete, concrete products and asphalt

• Essential element of almost every

construction project

• High margin & heavily integrated into

downstream solutions businesses

• Unique network of assets and expertise, a

trusted partner across our markets

… into value-added solutions that solve for ...

… Roads … Utility Infrastructure … and Outdoor Living

• Focused on publicly funded & resilient

infrastructure (highways, streets,

bridges, tunnels and intersections) with

significant investment needs

• Capability to adapt materials, products

and services as bespoke solutions

• Full-service, end-to-end offering across

the project lifecycle

• Solutions model provides higher quality

& better value to customers

• Focused on high-growth, critical utility

projects, water, energy and

communications networks

• Engineered systems to collect, protect

& connect vital utilities

• Highly specified & innovative solutions

for complex projects

• Value-added – design, specification,

manufacture, installation & maintenance

• Fully integrated with Essential Materials

and closely connected to Road

Solutions

• Focused on "Living Well Outside" with

innovative and bespoke products

including hardscapes, masonry,

fencing, railing, lawn and garden, pool

finishes and composite decking

• Provide customers with a full service

offering, from materials and products to

digital design services, technology and

logistics

• Strong track record with unmatched

depth of offering in high-growth markets

Annual Report 2023 iv

Chief Executive’s Letter to Shareholders and Stakeholders

Dear Shareholders and Stakeholders,

CRH’s differentiated strategy delivered a record financial performance in

2023 with further growth in profits, margins and cash generation.

This strong performance is testament to the hard work and enduring

commitment of the 78,500 people who work in CRH and make such a

significant contribution to our success.

It is also testament to the effectiveness of CRH's differentiated solutions

strategy in propelling our business to the next level of growth and

performance.

This is a time of significant opportunity for CRH to live our Purpose and

reinvent the way our world is built. This is why in 2023 we sought the

approval of our shareholders to change our primary stock market listing

arrangements and allow CRH to fully participate in the significant growth

opportunities that lie ahead.

Listing on NYSE

CRH first entered the U.S. market in 1978 and over the next five decades

has grown to become the largest building materials business in that market.

Since then, America’s continued economic expansion, growing population

and significant construction needs have been increasingly important drivers

of CRH’s business. Our Americas segments currently represent

approximately 75% of Adjusted EBITDA* and CRH continues to be uniquely

positioned to capitalize on the strong growth opportunities in the U.S.

construction market, underpinned by long-term structural tailwinds from

federal, state and municipal funding support.

On September 25, 2023 CRH successfully completed the transition of its

primary listing to the New York Stock Exchange (NYSE) following

overwhelming approval from shareholders at an Extraordinary General

Meeting (EGM) on June 8, 2023.

The Board and management of CRH believe a U.S. primary listing will bring

increased commercial, operational and acquisition opportunities for our

business, further accelerating our successful integrated solutions strategy

and delivering even higher levels of profitability, cash and returns for our

shareholders.

Improving Financial Performance

Over the last decade CRH has delivered industry-leading top and

bottom-line growth. We have increased our Adjusted EBITDA* threefold and

delivered ten consecutive years of margin improvement

5

.

4

We continued this trend in 2023, delivering a record financial performance

with total revenues increasing 7% to $34.9 billion (2022: $32.7 billion),

Adjusted EBITDA* of $6.2 billion (2022: $5.4 billion) up 15% and Adjusted

EBITDA margin*

6

increasing 120 basis points to 17.7% (2022: 16.5%).

Annual Report 2023 v

* Represents a non-GAAP measure. See the 'Non-GAAP Reconciliation' on pages xi to xiii.

5

Numbers based on IFRS financial reporting to 2022 and U.S. GAAP for 2023.

4

6

The GAAP figures which are most comparable to Adjusted EBITDA margin are: Net Income $3.1 billion (2022: $3.9 billion)/Total Revenues $34.9 billion (2022: $32.7 billion).

Delivering higher levels of

profitability, cash and returns for

our shareholders

Strong pricing, significant contributions from prior year acquisitions and good

underlying demand in key end-use markets offset the impact of cost inflation

reflecting our continued focus on commercial management and operational

efficiencies along with the benefits of our integrated solutions strategy.

Net debt*

7

of $5.4 billion at year end (2022: $3.9 billion) reflects continued

strong cash generation offset by disciplined capital expenditure,

value-focused investments and cash returns to shareholders.

Net income was $3.1 billion (2022: $3.9 billion), a decrease of $0.8 billion

driven by the absence of income from discontinued operations which

contributed $1.2 billion in 2022 due to the divestiture of the Building

Envelope business. Net income from continuing operations rose 14% to

$3.1 billion in 2023, which generated EPS of $4.36 (2022: $3.58). Excluding

the non-cash impairment charge EPS was $4.65, 30% higher than prior

year (2022: $3.58). This record financial performance combined with our

disciplined allocation of capital saw RONA*

8

for the year increase to 15.3%

(2022: 13.3%).

5,6,7

Capital Allocation and Development Activity

CRH repurchased $3.0 billion of shares in 2023 as part of its ongoing

buyback program. This demonstrates management’s confidence in the

outlook for our business and our continued strong cash generation, while

retaining the financial flexibility to invest in further growth and value creation

opportunities for our shareholders. As part of our dividend growth strategy

and in line with our strong financial position, the Board in November

increased the full year dividend to $1.33 per share, a 5% increase on the

prior year. Since 2018, CRH has returned approximately $12 billion to

shareholders through share buybacks and dividends.

CRH spent a total of $0.7 billion (2022: $3.3 billion) on acquisitions and

investments in 2023, the largest of which was Hydro International, a leading

provider of innovative stormwater products, wastewater treatment

products, wastewater services, and data solutions. This is a strategically

important acquisition for CRH, supporting our vision to be a leading provider

of solutions in the circular water economy and complementing our Building

& Infrastructure Solutions businesses in both North America and Europe.

In November, CRH reached an agreement to acquire an attractive portfolio

of cement and readymixed concrete assets in Texas for a total

consideration of $2.1 billion. The transaction was completed in February

2024, further strengthening our market leading position in Texas and

increasing our exposure to attractive, high-growth markets.

In February 2024, CRH entered into a binding agreement to acquire a

majority stake in Adbri Ltd (Adbri), a materials business in Australia. We will

acquire approximately 53% of the issued share capital for $0.7 billion,

increasing CRH’s total shareholding to approximately 57%. Adbri has high-

quality assets and leading market positions in Australia that complement

CRH’s core competencies in cement, concrete and aggregates while

creating additional opportunities for growth and development for our

existing Australian business. The proposed transaction is subject to

customary terms and conditions and is expected to complete in 2024.

CRH also entered into an agreement to divest its European lime operations

for a total consideration of $1.1 billion. The first phase of the divestment

completed in January 2024. The remaining phases consisting of operations

in the United Kingdom and Poland are expected to close in 2024. These

transactions demonstrate CRH’s active and disciplined approach to

portfolio management, and will provide significant additional capital

allocation opportunities to deliver further growth and value creation for our

shareholders.

Solutions Strategy

CRH transitioned to a new organisational structure on January 1, 2023 with

two regional Divisions and four new segments. This change accelerates the

development of our integrated solutions strategy in both the United States

and Europe as we align our business with the future growth opportunities of

our industry.

It will facilitate additional integration, cross-selling and joined up thinking

across CRH as we create value for our customers by combining our

products, materials and services, into solutions that solve some of the most

pressing construction problems.

Innovation

Investing in innovation that helps solve complex problems for customers is

part of our customer-centric approach to doing business. In Europe where

EU regulations are reshaping the way the built environment is constructed,

our businesses have both the impetus and opportunity to find new ways to

build better. This allows CRH to pilot and bring to market new products and

solutions that can then be rolled out to customers in North America as the

market evolves. In 2023 we continued to collaborate with customers and

other stakeholders from the built environment through our Innovation Centre

for Sustainable Construction and our venturing arm CRH Ventures.

Sustainability

Sustainability is deeply embedded in all aspects of our business. Our

sustainability framework identifies three global challenges for society and the

built environment - water, circularity and decarbonization. Our ability to

solve these challenges, by uniquely integrating our materials, products and

services, positions us to capture further value and accelerate growth across

CRH.

We continue to make progress on our industry-leading target to deliver a

30% reduction in absolute carbon emissions by 2030, keeping us on the

path to achieving our overall ambition of becoming a net-zero business by

2050. The Science Based Targets initiative (SBTi) has validated our 2030

emissions reduction targets

9

to be in line with a 1.5°C trajectory. CRH

continues to make progress against these targets reducing Scope 1 and 2

CO

2

e emissions by 8% in 2023.

We continue to keep the safety and well-being of our people as our utmost

priority and continue to provide our teams with the training and resources

needed to help ensure that everyone who works in CRH returns home

safely to their families at the end of the working day. Regrettably, despite

our efforts, CRH recorded four employee fatalities during the year. Our

thoughts are with their families and we will continue to do everything in our

power to reach our target of zero harm and zero fatalities.

Well Positioned for Future Growth

The success of CRH, our industry-leading financial performance and our

ability to deliver superior value for our customers is testament to the hard

work and commitment of all of our people. Their capabilities, combined with

the strength of our balance sheet and our relentless focus on the efficient

allocation of capital will enable us to capitalize on the significant

opportunities we see for further growth and value creation.

On behalf of the management team and all my colleagues across CRH, we

thank you for your continued support as we stand together to reinvent the

way our world is built.

Albert Manifold

Chief Executive

February 29, 2024

Annual Report 2023 vi

* Represents a non-GAAP measure. See the 'Non-GAAP Reconciliation' on pages xi to xiii.

7

Total debt of $11.6 billion (2022: $9.6 billion) is the GAAP figure which is most comparable to net debt.

5

8

Return on Net Segment Assets 14.4% (2022: 13.1%) is the GAAP figure which is most comparable to Return on Net Assets.

6

9

The SBTi’s Target Validation Team has determined that CRH’s target ambition for Scope 1 and Scope 2, as well as Scope 3 for purchased clinker and cement, is in line with a 1.5°C trajectory.

7

Why Invest in CRH?

Higher Profits, Cash and Returns

CRH is relentlessly focused on building better businesses through

operational and commercial excellence. Our differentiated strategy,

unmatched size and scale, and innovative and agile approach has driven

ten consecutive years of margin improvement.

In addition our financial discipline combined with industry-leading cash

generation enables us to invest for growth and increase cash returns to

shareholders. This approach has seen CRH increase its RONA* by over

900bps since 2013

10

and the Company sees strong potential for further

increases in the future.

8,9

Annual Report 2023 vii

* Represents a non-GAAP measure. See the 'Non-GAAP Reconciliation' on pages xi to xiii.

10

Numbers based on IFRS financial reporting to 2022 and U.S. GAAP for 2023.

8

11

The EPS numbers are presented on a continuing operations basis pre-impairment. Numbers based on IFRS financial reporting to 2020 and U.S. GAAP for 2021-2023.

9

Strong Earnings Growth

CRH has a strong track record of delivering for its shareholders.

Backed by its world-class management team, continued execution

of strategy and disciplined capital allocation, earnings per share has

more than doubled over the past five years. This has been driven by

CRH’s differentiated integrated solutions strategy, a deeply

embedded culture of continuous improvement and our efficient and

disciplined allocation of capital.

EPS Growth - Past Five Years

11

Consecutive years

of Margin

Improvement

10

RONA*

(2022: 13.3%)

Cumulative

Operating Cash Flow

last five years

10

Delivering consistent double-digit

growth

CRH has a strong track record of industry-leading financial performance and delivering superior value for shareholders. Since our foundation in 1970, CRH

has been relentlessly focused on building better businesses through operational and commercial excellence.

Over 50 years of superior delivery for shareholders

Combined with our financial strength and discipline, which are deeply embedded in our DNA, this differentiated strategy has consistently delivered higher

growth, profits, cash and returns on capital for our shareholders.

Shareholder Value Creation

Since formation in 1970 CRH has delivered an

industry leading annualized compound

long-term total shareholder return (TSR) of

15.7% (2022 14.8%).

Long-term TSR

1970 to 2023

15.7%

15.3%

$21bn

10

Powered by possibility and performance

Through its differentiated strategy, CRH has shaped its business to capitalize on the attractive fundamentals driving demand in high-growth construction

markets in North America and Europe.

Market Leading Positions

CRH is the market leader in many of the construction markets in which it

operates across North America and Europe. CRH prioritizes investment in

markets with attractive fundamentals including economic and population

growth, which in turn is driving demand for construction. In addition CRH is

a fully integrated building solutions provider which along with its unmatched

size and scale, leaves it uniquely positioned to capitalize on the growth

opportunities in these markets.

Differentiated Strategy

Our differentiated strategy is focused on uniquely integrating materials,

products and services across the construction value chain. We leverage our

scale, expertise and best practice to provide end-to-end solutions that solve

complex problems for our customers. We utilize specific expertise in areas

such as materials science, design and engineering to innovate and create

new products that don't yet exist. This allows us to do more for our

customers and help deliver a higher performing and more sustainable built

environment.

Performance-Focused Operator

CRH has the ability to leverage its high performing assets in the most

attractive markets to generate industry-leading profits, cash and returns.

This ability is underpinned by a differentiated strategy delivered by an

experienced management team with deep industry experience and a

proven track record of consistent financial and operational delivery.

Innovation and Sustainability

Sustainability is deeply embedded in all aspects of our business. We create

value by uniquely integrating our materials, products and services to offer

more innovative solutions for our customers and advance our progress in

water, circularity and decarbonization. For example, CRH is a significant

contributor to the circular economy and in 2023 we recycled 43.9m tonnes

of by-products and wastes from other industries enabling us to preserve our

finite natural resources and extend the life of our reserves.

Annual Report 2023 viii

Our strong and flexible balance sheet provides CRH with

significant financial capacity for long-term value creation

through accretive M&A, expansionary capital expenditure

and cash returns to shareholders through dividends and

share buybacks. Since 2018 CRH has allocated

approximately $28 billion across these areas. CRH aims to

significantly increase its financial capacity in the years

ahead and continue to allocate capital for future growth

and superior shareholder value creation.

$5bn

Dividends

$13bn

M&A

$7bn

Buybacks

$3bn

Exp. Capex

$28bn

Capital Allocation

since 2018

Balance Sheet Strength

Well positioned for future growth and value creation

CRH has identified three specific growth drivers that will shape the performance of its business and the value it creates for shareholders.

Organic Growth

Across both our major markets, North America and Europe, we see

significant growth potential driven by unprecedented funding for

infrastructure, increased investment in critical utilities and reindustrialization,

and a structural housing deficit. The European market is supported by a

number of region-wide funding programs including the Green Deal, which is

part funded through the NextGenerationEU programme (€800 billion), and

the Chips for Europe Initiative. In North America, these end-markets are

underpinned by Federal stimulus including the Infrastructure Investment and

Jobs Act ($1.2 trillion), the Inflation Reduction Act ($370 billion) and the

CHIPS and Science Act ($280 billion). CRH is the largest building materials

player in North America and is ideally positioned to be a leading beneficiary

of this golden age for construction.

10

Inorganic Growth

In 2023, CRH spent a total of $0.7 billion (2022: $3.3 billion) on acquisitions

and investments. We have a proven track record in value creation through

acquisitions which historically have accounted for approximately two-thirds

of CRH’s growth. We achieve this by acquiring businesses at attractive

valuations and creating value by integrating them with our existing

operations and generating synergies. The Company’s cash generation

capability underpins our financial capacity for accretive M&A, growth

investments and further cash returns to shareholders.

Innovation and Agility

As the nature of construction and the needs of our customers and society

changes, CRH’s agility and ability to innovate are critical growth drivers.

CRH has a strong track record in this area over the past 10 years,

innovating to develop new materials, products and services to help solve

our customers’ complex construction problems. Our strategy transforms

essential materials into value-added and innovative sustainable solutions to

address the changing needs of construction.

Annual Report 2023 ix

* Represents a non-GAAP measure. See the 'Non-GAAP Reconciliation' on pages xi to xiii

12

The Company’s ability to deliver on its ambitions is dependent on it achieving its planning assumptions, which may be negatively impacted by adverse changes in economic conditions in the

countries where the Company operates, a slowdown in growth of the overall construction and building materials sector or changes in availability of public funding for infrastructure, and other

factors discussed under the heading “Risk Factors” in the Company's 2023 Annual Report on Form 10-K as filed with the United States Securities and Exchange Commission.

10

Our ambition: A double-digit growth company through the cycle

12

$1.9 Trillion

$1.2tn

U.S. Infrastructure Investment

and Jobs Act

$370bn

U.S. Inflation Reduction Act

$280bn

U.S. CHIPS and Science Act

Leading the transition to smarter, better connected and more sustainable construction

Innovation and Sustainability

At CRH, we provide solutions to some of the most complex and technically challenging construction projects in the world. We have the capabilities and the expertise

to provide our customers with the innovative, value-added solutions they need by integrating materials, products, and services over the entire project lifecycle. We are

constantly innovating to improve existing and develop new technologies that will address the changing needs of construction and provide us with a platform for future

growth. Through our Innovation Center for Sustainable Construction, we have a global network of experts across our businesses collaborating in the research,

development and replication of innovative solutions. In addition, our CRH Ventures platform works in partnership with industry players and academic institutions to pilot

and scale cutting-edge and innovative technologies.

We believe the transition to a more sustainable built environment is a significant commercial opportunity for CRH. We are well positioned to capitalize on increased

demand for more sustainable solutions, which is underpinned by significant U.S. and EU funding programs and regulatory policies. Our ability to replicate and scale our

innovation and technical expertise between Europe and North America gives us opportunities for further growth. As our customers’ needs continue to evolve, our

solutions help them to build better, quicker, safer, and more sustainably.

Our Sustainability Framework identifies three rapidly emerging and hard to solve global challenges for society and the built environment that CRH can help to solve:

water, circularity and decarbonization. We are uniquely placed to provide value driven solutions to help solve these challenges, designing and innovating our products,

services and solutions to capture further value and accelerate growth across CRH. In addition, we continue to invest in our strong sustainability foundations: protecting

the natural world, helping our people and communities to thrive and ensuring we operate as a responsible business.

11,12

Another year of progress

Creating value through our sustainable solutions

#1

43.9m tonnes

0.9kg/$ Revenue

The largest recycler in

North America

wastes and by-products from other

industries recycled in 2023 (2022:

42.4mt)

CO

2

e emissions per dollar of

revenue in 2023

14

(2022: 1.0kg/$ Revenue)

Executing against our 2030 target to deliver a 30% reduction in absolute CO

2

e emissions

8% 36% 1.5°C

reduction in Scope 1

and 2 CO

2

e

emissions in 2023

alternative fuels used in our cement

plants

aligned 2030 targets

validated by SBTi

Innovating to accelerate our solutions strategy

Enhancing our capabilities

The acquisition of Hydro International

expands our stormwater and wastewater

treatment products, services, and data

solutions. In Romania CRH launched a

first-of-its-kind co-processing facility,

processing non-recyclable waste into

alternative fuels, contributing to the circular

economy.

Partnering with start-ups

Through our $250 million Venturing and

Innovation Fund we are investing in

construction and climate technology

start-ups to form bold new partnerships. The

CRH Ventures Accelerator for Water

Solutions advances the most promising

solutions that address the challenges of

water management.

Investing in innovative technologies

Across our Road Solutions business, we are

progressing trials with alternative binders

that improve performance, durability and

increase recycled asphalt content. Our water

infrastructure business is partnering with

artificial intelligence and technology solutions

provider, FIDO Tech, to deliver unparalleled

leak detection and water conservation

solutions in the United States.

Annual Report 2023 x

13

Revenue derived from products that incorporate any, or a combination of; recycled materials; are produced using alternative energy and fuel sources; have a lower-carbon footprint as

compared to those produced using traditional manufacturing processes; and/or are designed to specifically benefit the environment (i.e. water treatment and management systems, products

with strong thermal mass/U-values).

11

14

Scope 1 and 2 CO

2

e emissions (kg/$ revenue). CO

2

e emissions subject to final verification under the European Union Emissions Trading System (EU ETS).

12

9.4

11.4

12.6

13.9

2020 2021 2022

2023

Revenue from products with enhanced

sustainability attributes

13

($ billion)

48

47

44

34

2021 2022 2023 2030 target

Total CO

2

e emissions (mt)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2023

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 001-32846

CRH public limited company

(Exact name of registrant as specified in its charter)

Republic of Ireland 98-0366809

(State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification Number)

Stonemason’s Way, Rathfarnham, Dublin 16, D16 KH51, Ireland

+353 1 404 1000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class: Trading Symbol: Name of Each Exchange on Which Registered:

Ordinary Shares of €0.32 each

6.40% notes due 2033

CRH

New York Stock Exchange

New York Stock Exchange

CRH/33A

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒Yes☐

No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange

Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the

Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted

pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period

that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller

reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,”

“smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☒ Accelerated filer ☐

Non-accelerated filer ☐ Smaller reporting company ☐

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period

for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the

effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes Oxley Act (15 U.S.C 7262(b))

by the registered public accounting firm that prepared or issued its audit report. ☒Yes ☐ No

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the

registrant included in the filing reflect the correction of an error to previously issued financial statements. □

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-

based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to

§240.10D-1(b). □

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐Yes ☒ No

The aggregate market value of the voting shares held by non-affiliates of the registrant, computed by reference to the closing

price as reported on the New York Stock Exchange, as of the last business day of CRH plc’s most recently completed

second fiscal quarter (June 30, 2023), was $40,589,313,781. CRH plc has no non-voting common equity.

As of February 15, 2024, the number of outstanding ordinary shares was 690,357,372.

Documents Incorporated by Reference: None.

EXPLANATORY NOTE

CRH plc (together with its consolidated subsidiaries, the “Company”, “CRH”, the “Group”, “we”, “us” or “our”), a corporation

organized under the laws of the Republic of Ireland, is a foreign private issuer in the United States for purposes of the

Securities Exchange Act of 1934, as amended (the “Exchange Act”). CRH voluntarily has chosen to file annual reports on

Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K with the United States Securities and Exchange

Commission (SEC) instead of filing on the reporting forms available to foreign private issuers.

TABLE OF CONTENTS

PART I PAGE

Item 1 Business 3

Item 1A Risk Factors 10

Item 1B Unresolved Staff Comments 16

Item 1C Cybersecurity 17

Item 2 Properties 18

Item 3 Legal Proceedings 24

Item 4 Mine Safety Disclosures 24

PART II

Item 5 Market for Registrants Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities 25

Item 6 Reserved 27

Item 7 Management's Discussion and Analysis of Financial Condition and Results of Operations 28

Item 7A Quantitative and Qualitative Disclosures about Market Risk 47

Item 8 Financial Statements and Supplementary Data 48

Item 9 Changes in and Disagreements with Accountants on Accounting and Financial Disclosures 100

Item 9A Controls and Procedures 100

Item 9B Other Information 101

Item 9C Disclosures Regarding Foreign Jurisdictions that Prevent Inspections 101

PART III

Item 10 Directors, Executive Officers and Corporate Governance 102

Item 11 Executive Compensation 102

Item 12 Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters 102

Item 13 Certain Relationships and Related Transactions, and Director Independence 102

Item 14 Principal Accountant Fees and Services 102

PART IV

Item 15 Exhibits and Financial Statement Schedules 103

Item 16 Form 10-K Summary 104

Signatures 105

CRH Form 10-K 1

Forward Looking Statements – Safe Harbor Provisions Under The Private Securities Litigation Reform Act Of

1995

In order to utilize the “Safe Harbor” provisions of the United States Private Securities Litigation Reform Act of 1995, CRH is providing the following cautionary

statement.

This document contains statements that are, or may be deemed to be, forward-looking statements with respect to the financial condition, results of

operations, business, viability and future performance of CRH and certain of the plans and objectives of CRH. These forward-looking statements may

generally, but not always, be identified by the use of words such as “will”, “anticipates”, “should”, “could”, “would”, “targets”, “aims”, “may”, “continues”,

“expects”, “is expected to”, “estimates”, “believes”, “intends” or similar expressions. These forward-looking statements include all matters that are not

historical facts or matters of fact at the date of this document.

In particular, the following, among other statements, are all forward-looking in nature: plans and expectations regarding customer demand, pricing, costs,

underlying drivers for growth in infrastructure, residential and non-residential activity, and macroeconomic and other trends in CRH’s markets, including

onshoring, regulatory trends, and investment in technology, clean energy and manufacturing; plans and expectations regarding government funding initiatives

and priorities, including the timing and amount of government funding and its effects on CRH’s business; plans and expectations regarding CRH’s strategy,

expansionary capital expenditures, competitive advantages, growth opportunities, innovation, research and development and acquisitions and divestments,

including the timing for completion, tax and accounting effects and expected commercial benefits; plans and expectations regarding the outcome of pending

legal proceedings and provisions for environmental and remediation costs; plans and expectations regarding the timing and amount of share buybacks and

dividends, including the Board’s policy of consistent long-term dividend growth; expectations regarding taxation of U.S. holders of our shares, including

applicability of Irish Dividend Withholding Tax (DWT) and Irish stamp duty; expectations regarding the Company’s income tax reserves and returns; plans and

expectations regarding equity incentive plans and pension plans; plans and expectations regarding CRH’s balance sheet, capital allocation, financial capacity,

accounting policies, cash flows and working capital; expectations regarding CRH’s ability to fund its long-term contractual obligations, maturing debt

obligations, capital expenditures; and other liquidity requirements, plans and expectations regarding the amortization of costs related to issuance of debt in

2023 and recognition of compensation expense related to the Share Option Schemes; plans and expectations regarding the expected benefits of CRH’s

primary listing on the New York Stock Exchange (NYSE); plans and expectations regarding the effect of existing and future laws, rules and regulations on

CRH’s business; plans and expectations regarding human capital initiatives, workplace safety, sustainability and climate change, CRH’s decarbonization

targets, sustainability-related initiatives and business opportunities, including investments, and the delivery of and consumer demand for sustainable solutions

and products; and plans and expectations regarding the potential impact and evolving nature of risks and CRH’s management of such risks.

By their nature, forward-looking statements involve risk and uncertainty because they relate to events and depend on circumstances that may or may not

occur in the future and reflect the Company’s current expectations and assumptions as to such future events and circumstances that may not prove

accurate. You are cautioned not to place undue reliance on any forward-looking statements. These forward-looking statements are made as of the date of

this document. The Company expressly disclaims any obligation or undertaking to publicly update or revise these forward-looking statements other than as

required by applicable law.

A number of material factors could cause actual results and developments to differ materially from those expressed or implied by these forward-looking

statements, certain of which are beyond our control, and which include, among other factors: economic and financial conditions, including changes in

interest rates, inflation, price volatility and/or labor and materials shortages; demand for infrastructure, residential and non-residential construction and our

products in geographic markets in which we operate; increased competition and its impact on prices and market position; increases in energy, labor and/or

other raw materials costs; adverse changes to laws and regulations, including in relation to climate change; the impact of unfavorable weather; investor and/

or consumer sentiment regarding the importance of sustainable practices and products; availability of public sector funding for infrastructure programs;

political uncertainty, including as a result of political and social conditions in the jurisdictions CRH operates in, or adverse political developments, including the

ongoing geopolitical conflicts in Ukraine and the Middle East; failure to complete or successfully integrate acquisitions or make timely divestments; cyber-

attacks and exposure of associates, contractors, customers, suppliers and other individuals to health and safety risks, including due to product failures.

Additional factors, risks and uncertainties that could cause actual outcomes and results to be materially different from those expressed by the forward-

looking statements in this report including, but not limited to, the risks and uncertainties described herein and in “Risk Factors” in Part 1, Item 1A of this

Annual Report on Form 10-K for the year ended December 31, 2023 (the “Annual Report on Form 10-K”).

CRH Form 10-K 2

PART I

Item 1. Business

Overview

CRH is a leading provider of building materials solutions that build, connect and improve our world. In 2023, the Company generated $34.9 billion of

revenues, $3.1 billion of net income and $6.2 billion of Adjusted EBITDA*.

1

Since formation in 1970, CRH has evolved from being a supplier of base materials

to providing end-to-end value-added solutions that solve complex construction challenges for our customers. CRH works closely with the customer across

the entire project lifecycle from planning, design, manufacture, installation and maintenance through to end-of-life recycling, using our engineering and

innovation expertise to provide superior materials, products and services.

The Company integrates essential materials (aggregates and cement), value-added building products as well as construction services, to provide our

customers with complete end-to-end solutions. CRH’s capabilities, innovation and technical expertise enable it to be a valuable partner for transportation and

critical utility infrastructure projects, complex non-residential construction and outdoor living solutions.

CRH’s business addresses the needs of customers across infrastructure, non-residential and residential construction markets. In 2023, approximately 35%

of revenues came from infrastructure (such as highways, streets, roads, bridges, and critical utility infrastructure), 30% from non-residential construction

(including construction and maintenance of manufacturing, datacenter and distribution facilities) and 35% from residential construction. 55% of revenues

came from sales to new-build construction, while 45% of revenues came from repair and remodel activity.

Operating in 29 countries, the Company has market leadership positions in North America and Europe. In 2023, 72% of net income and 73% of Adjusted

EBITDA* was generated in North America. The United States is expected to be a key driver of future growth for CRH due to continued economic expansion,

a growing population and significant public investment in construction. Our European business, which benefits from strong economic and construction

growth prospects across Central and Eastern Europe as well as recurring repair and remodel demand in Western Europe, is an important strategic part of the

Company and CRH intends to continue to expand its operations across the region. In both geographies there is significant government support for

infrastructure and increasing demand for integrated solutions in major infrastructure and commercial projects.

CRH has a proven track record in value creation through acquisition which over the last decade has accounted for approximately two-thirds of the

Company’s growth. We achieve this by acquiring businesses at attractive valuations and creating value by integrating them with our existing operations and

generating synergies. The Company takes an active approach to portfolio management and continuously reviews the competitive landscape for attractive

investment and divestiture opportunities to deliver further growth and value creation for shareholders. In 2023, CRH completed 22 acquisitions for a total

consideration of $0.7 billion compared with $3.3 billion in 2022. The largest acquisition in 2023 was in our Americas Building Solutions segment where the

Company completed the acquisition of Hydro International, a leading provider of stormwater and wastewater solutions in North America and Europe.

In 2023, CRH transitioned its primary stock exchange listing from the London Stock Exchange (LSE) to the NYSE. CRH currently maintains a primary listing

on the NYSE and a standard listing on the LSE for its ordinary shares, each listing represented by the ticker symbol “CRH”. CRH believes that its NYSE

primary listing will bring increased commercial, operational and acquisition opportunities for the Company, further accelerating its integrated solutions strategy

and delivering even higher levels of profitability, cash and returns for its shareholders.

Customer Solutions

CRH’s differentiated strategy integrates building materials, products and services by providing them to customers as complete solutions that solve key

challenges across the built environment.

Essential Materials

Essential Materials, consisting of aggregates and cement, are the foundation of CRH’s solutions strategy. Our vertically integrated businesses manufacture

and supply these materials for use extensively in a wide range of construction applications, ranging from major road and infrastructure projects to the

development and refurbishment of commercial buildings, private residences, public spaces and communities. Our deep materials and market knowledge,

along with our extensive network of locations and assets, drives our performance and helps us deliver value to our customers. Customers typically range

from national, regional and local governments to contractors and other construction product and service providers.

Road Solutions

CRH is a leading provider of solutions for sustainable road construction in North America and Europe. With our capabilities in manufacturing, installation,

maintenance and circularity, we deliver a range of innovative solutions for our customers to better connect our communities, from major public highway

infrastructure projects to residential roads, airports and parking lots. As responsible operators considerate of our environmental impact, we optimize the use

of recycled materials in our paving services, thereby reducing waste, emissions and energy consumption. Fully integrated with our Essential Materials

businesses, we have developed our Road Solutions offering to provide customers with quality, flexibility, speed, expertise and convenience through our deep

market knowledge and highly capable team of professionals.

Building and Infrastructure Solutions

Our Building & Infrastructure Solutions connect, protect and transport critical water, energy and telecommunications infrastructure to help solve complex

construction challenges. We integrate design, materials, products and engineering to enable the transition to a more sustainable and resilient built

environment with a particular focus on the below-ground built environment where we are a leading provider of multi-material infrastructure that connects and

protects the critical utilities that enhance the daily lives of millions of people.

CRH Form 10-K 3

* Represents a non-GAAP measure. See the discussion within 'Non-GAAP Reconciliation and Supplementary Information' on pages 38 to 40.

1

Outdoor Living Solutions

CRH’s Outdoor Living Solutions integrate specialized materials, products and design features to enhance the quality of private and public spaces. We help

our customers in residential and commercial markets create unique outdoor settings by providing solutions for repair, remodel and new construction projects.

Our business is closely connected to our customers through a broad geographic network as well as a comprehensive suite of products and services

spanning hardscapes, masonry, fencing, railing, packaged lawn and garden products, pool finishes and composite decking. We place a strong focus on

anticipating the needs of our customers and constantly strive to exceed their expectations. We do this by continually enhancing our offering through

innovation, portfolio expansion and multifaceted collaboration.

Innovation and Sustainability

We are accelerating investment in innovation to develop a higher-performing and more sustainable built environment. Through our $250 million Venturing and

Innovation Fund we are supporting the development of new technologies and innovative solutions to meet the increasingly complex needs of customers and

evolving trends in construction. Our ability to replicate and scale our innovation and technical expertise between Europe and North America provides us with

opportunities for further growth. Through our Innovation Center for Sustainable Construction (ICSC), we have a global network of experts across our

businesses collaborating in the research, development and replication of innovative solutions. In addition, our CRH Ventures platform works in partnership

with industrial leaders (such as Shell, Volvo, Caterpillar and others) and academic institutions to pilot and scale cutting-edge and innovative technologies.

Sustainability is deeply embedded in all aspects of our business and sustainability leadership is a key pillar of CRH’s purpose. CRH’s building materials

solutions play an important role in shaping a more sustainable built environment and in 2023, revenues from products with enhanced sustainability attributes

1

was $13.9 billion, an increase of 10% compared with 2022 and an increase of 22% compared with 2021.

Our sustainability framework identifies three global challenges for society and the built environment; water, circularity and decarbonization. Our ability to solve

these challenges by uniquely integrating our materials, products and services, positions us to capture further value and accelerate growth across CRH.

• Water: We are advancing solutions to address global water challenges by enhancing flood resilience and improving water management. This includes

upgrading water infrastructure, improving wastewater treatment, recharging groundwater and conserving water across the supply chain.

• Circularity: We are reimagining the way materials are used to enable a more circular economy. Our efforts include preserving natural resources,

recycling and reusing construction and waste materials, facilitating resource-efficient buildings and infrastructure and building more circular supply

chains.

• Decarbonization: We are developing innovative solutions to support a low-carbon future. Our goals include reducing our absolute carbon emissions,

minimizing operational carbon from our products and creating energy-efficient solutions to facilitate the clean energy transition.

By continuing to meet the changing needs of our customers and society, we aim to drive further growth and value creation. In addition, we are striving to

create a positive impact on the natural world, helping our people and communities to thrive. We stand out as a responsible business by collaborating to

ensure a more sustainable supply chain and embedding responsible conduct at each level throughout our organization.

Business Segment Information

In the year ended December 31, 2023, CRH was organized through four segments across two divisions.

Americas Division

CRH’s Americas Division comprises two segments: Americas Materials Solutions and Americas Building Solutions. The North American market’s positive

fundamentals, including strong population growth and significant public investment in construction, is driving demand for CRH’s materials, products and

services. Over several decades, CRH has established leadership positions across the United States and Canada. The Division employs approximately 46,400

people at 1,949 locations across 48 states of the United States and seven Canadian provinces.

Americas Materials Solutions

Americas Materials Solutions provides building materials for the construction and maintenance of public infrastructure and commercial and residential

buildings in North America. The primary materials produced by this segment include aggregates, cement, readymixed concrete and asphalt. This segment

also provides paving and construction services for customers.

In 2023, this segment accounted for approximately 44% of CRH’s total revenues and 50% of Adjusted EBITDA. Approximately 50% of segment revenues

came from infrastructure, 30% from non-residential construction and 20% from residential construction. New-build construction accounts for approximately

50% of segment revenues while the remaining 50% came from repair and remodel activity.

The Americas Materials Solutions segment leverages our strong market knowledge, deep industry expertise and extensive array of essential materials to

implement CRH’s differentiated strategy, offering value-added, end-to-end solutions which combine different types of materials, products and services to

satisfy multiple customer needs. In turn, this enables CRH to provide a value-enhancing, one-stop-shop experience, saving time and reducing logistical

complexity for customers. Through this approach CRH aims to reduce lead times and complexity, deepening relationships, driving repeat business and

increasing the share of customer wallet spent on CRH products and services.

Vertical integration is a defining characteristic within this segment, enabling us to optimize production throughout the value chain and to capture greater

value. In order to support its operations, the Company has established a network of long-term reserves at quarry locations, predominantly adjacent to urban

areas where demand for its materials and products is strongest.

Americas Building Solutions

Americas Building Solutions manufactures, supplies and delivers high quality, value-added, innovative solutions for the built environment in communities

across North America. Solutions in this segment are highly specified, designed and engineered thereby adding value for the customer. This segment offers

solutions serving complex critical utility infrastructure (such as water, energy, transportation and telecommunications projects) and outdoor living solutions for

enhancing private and public spaces.

CRH Form 10-K 4

1

Revenues from products with enhanced sustainability attributes is defined as revenues derived from those products that incorporate any, or a combination of; recycled materials; are produced

using alternative energy and fuel sources; have a lower carbon footprint as compared to those products using traditional manufacturing processes; and are designed to specifically benefit the

environment.

In 2023, Americas Building Solutions accounted for approximately 20% of CRH’s total revenues and 23% of Adjusted EBITDA. Approximately 65% of

segment revenues came from sales to residential, 25% to the non-residential market and 10% to infrastructure. Repair and remodel activity accounted for

approximately 60% of segment revenues, with the remaining 40% from new-build construction.

This segment analyzes market trends, including increasing urbanization, demand for more sustainable construction and evolving customer preferences to

devise high quality, effective building product solutions. CRH’s ability to provide end-to-end solutions which are tailored to the specific requirements of

individual customer projects helps to drive competitive advantage and deliver sustainable growth in this segment.

Europe Division

CRH’s Europe Division comprises two segments: Europe Materials Solutions and Europe Building Solutions. In Eastern Europe, we see high growth potential

through strong infrastructure activity underpinned by European Union (EU) funding mechanisms. In Western Europe, CRH’s businesses operate in markets

which are more stable and developed with resilient demand for repair and remodel activity. In both regions, CRH is experiencing increasing demand for its

integrated end-to-end solutions offering. The Division employs approximately 32,100 people at 1,441 locations across 28 countries.

Europe Materials Solutions

Europe Materials Solutions provides building materials for the construction of public infrastructure and commercial and residential buildings across Europe.

The primary materials produced in this segment include aggregates, cement, readymixed concrete, asphalt and concrete products.

In 2023, this segment accounted for 28% of CRH’s total revenues and 22% of Adjusted EBITDA. Approximately 35% of segment revenues came from

infrastructure, 35% from residential construction, and 30% from non-residential construction. New-build construction accounted for approximately 65% of

segment revenues, with the remaining 35% from repair and remodel activity.

The segment has extensively integrated its operations, enabling it to provide essential materials, value-added products and services and complete solutions

to customers. CRH has established itself as a market leader through this integrated approach, particularly in European regions, where the Company’s

cement, readymixed concrete and aggregates operations have been integrated with its precast and concrete products businesses, enabling strong value

creation through commercial excellence and performance improvement initiatives.

Europe Building Solutions

Europe Building Solutions combines materials, products and services to produce a wide range of architectural and infrastructural solutions for use in the

building and renovation of critical utility infrastructure, commercial and residential buildings and outdoor living spaces. This business serves the growing

demand across the construction value chain for innovative and value-added products and services.

In 2023, this segment accounted for 8% of CRH’s total revenues and 5% of Adjusted EBITDA. Approximately 40% of segment revenues came from

residential construction, 35% from non-residential construction, and 25% from infrastructure. New-build construction accounted for approximately 80% of

segment revenues, with the remaining 20% from repair and remodel activity.

This business integrates design, engineering, materials and products to enable the transition to a more sustainable and resilient built environment.

Materials and Products

The following materials and products are produced and supplied by CRH’s businesses.

Aggregates

Aggregates are naturally occurring mineral deposits such as granite, limestone and sandstone. CRH extracts these deposits and processes them for sale as

aggregates products such as sand, gravel, and crushed stone. Typically, aggregates are used in road and rail infrastructure, building foundations and in the

production of products including concrete and asphalt. Annualized aggregates sales volumes

2

in 2023 for the Americas Division and Europe Division were

213.9 million tons and 104.0 million tons, respectively.

Cement

Cement is produced from limestone reserves and is the primary binding agent in the production of concrete products, including readymixed concrete and

mortars, which are used extensively throughout the built environment. Annualized cement sales volumes

2

in 2023 for the Americas Division and Europe

Division were 13.4 million tons and 30.9 million tons, respectively.

Concrete

Concrete is a highly versatile building material, comprised of aggregates bound together with cement and water. Readymixed concrete is the most commonly

used form of concrete. It forms the foundations of buildings and homes, roads, tunnels and bridges, water management systems and clean energy

structures. While readymixed concrete is supplied to customers for on-site casting, CRH’s infrastructural concrete businesses produce and supply precast

and pre-stressed concrete products such as floor and wall elements, beams and vaults, pipes and manholes. These products are delivered to, and

assembled at, construction sites where they are used throughout the modern built environment. Annualized readymixed concrete sales volumes

2

in 2023 for

the Americas Division and Europe Division were 16.1 million cubic yards and 18.3 million cubic yards, respectively.

Asphalt

Asphalt consists of aggregates bound together with bitumen and is widely used as a surface material in roads, bridges, airport runways, sidewalks and other

amenities. In recent years, the use of recycled materials in asphalt has increased considerably. Using materials from existing road surfaces to produce new

asphalt reduces the need for virgin material demand, extends the life of our aggregates reserves and contributes to reducing the carbon footprint of the

product. Recycled Asphalt Pavement (RAP) and Recycled Asphalt Shingles (RAS) are used extensively by CRH businesses to produce new asphalt products

for road and other surfaces. Annualized asphalt sales volumes

2

in 2023 for the Americas Division and Europe Division were 52.5 million tons and 10.2 million

tons, respectively.

CRH Form 10-K 5

2

Annualized sales volumes reflect the full-year impact of acquisitions and divestitures during the year and may vary from actual volumes sold.

Building Products

CRH’s Building & Infrastructure Solutions businesses manufacture concrete and polymer-based products such as underground vaults, drainage systems,

utility enclosures and modular precast structures which are typically supplied to the water, energy, telecommunications and railroad markets. The businesses

also provide a range of engineered steel and polymer-based anchoring, fixing and connecting solutions for a variety of new-build construction applications.

CRH’s Outdoor Living Solutions businesses manufactures a variety of concrete masonry, hardscape and related products including pavers, blocks and

curbs, retaining walls and slabs. The businesses also produces fencing and railing systems, composite decking, lawn and garden products and packaged

concrete mixes. These products are supplied to residential, commercial & do-it-yourself (DIY) construction markets.

Key Trends and Opportunities

Key trends affecting the development of CRH's business include:

• Population growth and urbanization driving increasing demand for construction;

• Economic development and further investment in infrastructure, commercial and residential projects; and

• Recurring need to repair, maintain and upgrade the built environment as existing buildings and infrastructure age and wear.

In addition, there are several industry-specific trends that are shaping how CRH evolves to meet the needs of its customers:

• Unprecedented levels of funding support for infrastructure, critical utilities and the onshoring of manufacturing activity;

• An evolving regulatory landscape driving increasing customer demand for innovative, end-to-end solutions to deliver a more resilient and sustainable

built environment; and

• Supply-side dynamics, such as labor constraints, driving increasing investment in automation, technology and digital solutions.

Environmental and Governmental

Regulations

Our operations in the United States are subject to federal, state and local laws, while our European operations are primarily subject to national environmental

laws and regulations stemming primarily from EU directives and regulations. Our operations elsewhere are typically subject to both national and local

regulatory requirements.

Compliance and Costs

Compliance with applicable regulations requires capital investment and ongoing expenditures for the operation and maintenance of systems and

implementation of improvement programs. These include investments in licensing, permitting and monitoring, waste and water management plans,

reductions in air emissions and energy consumption, promotion and protection of biodiversity, education and training, as well as employment of

environmental specialists within CRH. These capital investments and expenditures were not material to CRH’s earnings, results of operations or financial

condition in 2023 and 2022.

Management believes that its current provision for environmental and remediation costs is reasonable and that any potential non-compliance at its operations

and facilities with applicable environmental laws and regulations is not likely to have a material adverse effect on CRH’s operations or financial condition. See

Item 3. “Legal Proceedings" and Note 13 “Asset retirement obligations” in Item 8. “Financial Statements and Supplementary Data” of this Annual Report on

Form 10-K.

Land and Environmental Management

We generally own or lease the real estate on which our main raw materials, aggregates and other minerals are located. As part of our vertically integrated

business model, we have established an extensive global network of quarries comprised of 1,235 properties, of which 226,153 hectares of land are owned

and 97,046 hectares are leased. These quarries provide us with the raw materials to manufacture various primary building materials, such as aggregates,

cement, asphalt, readymixed concrete and concrete products. We offer these products directly for sale and integrate them into our downstream products

and services. Materials produced by our aggregates and cement businesses, for example, can be supplied to our downstream businesses for use in our

Road Solutions, Outdoor Living Solutions and Building & Infrastructure Solutions businesses.

Our operations are typically required to comply with government land use plans and zoning requirements. We are required by government authorities to

obtain permits to operate certain workplaces, such as quarries, mines, production and distribution facilities, including water rights required to operate many

of our sites. The terms and general availability of government permits required to conduct our business influence the scope of our operations on the

respective sites. We are also required to obtain permits and adhere to applicable restrictions, often including establishing appropriate environmental

management systems, to minimize the risk that necessary permits are revoked, modified or not renewed.

CRH is also subject to multiple laws that require the Company, as a mine operator, to reclaim and restore properties after mining activities have ceased. As a

result we are required to record reasonable provisions for such reclamation in our Consolidated Financial Statements.

From time to time, we are required by law and/or contractual obligations to investigate and remediate releases of hazardous substances at our manufacturing

sites and at sites where hazardous substances from our operations may have been disposed of. Where we have been required to incur such expenses, we

are required to record reasonable provisions for such remediation in our Consolidated Financial Statements.

The Clean Air Act in the United States and similar laws elsewhere require that certain of our facilities, including our cement plants, obtain and maintain air

emissions permits that subject them to pollution control requirements and require pre-approval for constructing certain facilities. CRH is also required to

comply with laws designed to promote biodiversity and protect ecosystems. From time to time, CRH may be required to install additional equipment or

technologies to remain in compliance with such environmental regulations.

CRH Form 10-K 6

Climate Change

We believe the transition to a more sustainable built environment represents a commercial opportunity for CRH. Certain government legislation designed to

accelerate the energy transition has had a positive impact on our business and we see increasing opportunities as public policy changes begin to increase

demand for low-carbon, sustainable products. We are well-positioned to capitalize on this increased demand, which is underpinned by significant United States

and EU funding programs and regulatory policies. In particular, the $1.2 trillion Infrastructure Investment and Jobs Act (IIJA) is the single largest long-term

infrastructure investment in the history of the United States. In 2023, CRH’s operating companies across the United States helped to deliver multiple

infrastructure projects receiving funding under the IIJA.

As part of our ambition to be a net-zero business by 2050, CRH has announced an absolute carbon dioxide (CO

2

) emissions reduction target of 30% by

2030 (from a 2021 base year) inclusive of organic business growth. The Science Based Targets initiative (SBTi) has validated our targets

3

in line with a 1.5°C

trajectory. A significant portion of the actions required to deliver on the 2030 roadmap are based on known technologies, well-established operational

excellence programs and activities in which CRH has a proven track record of delivery. CRH’s roadmap includes incremental capital expenditure of

approximately $150 million per annum on average, which is subject to strict internal investment criteria and the net business benefit is expected to increase

revenues and profitability.

In 2023, our Scope 1 and 2 absolute carbon emissions decreased by 8%, from 33.6 million tonnes

4

in 2022 to 31.0 million tonnes in 2023, as we executed

against the levers in our decarbonization roadmap and benefited from lower clinker production. Our cement-specific net CO

2

emissions per tonne of

cementitious product amounted to 562kg (566kg in 2022). We are also continuing to advance our contribution to the circular economy, preserving scarce

natural resources and using more recycled materials in construction. In 2023, we recycled 43.9 million tonnes of by-products and wastes from other

industries as raw materials and fuels in our products and processes (42.4 million tonnes in 2022).

CRH will continue to invest in solutions that strengthen circularity and resilience to climate change in the built environment.

Supply Chain

CRH employs a dedicated global purchasing team and its supply chain combines vertical integration as well as external suppliers and service providers to

deliver products to customers in various markets.

As outlined on page 6, CRH owns or leases the real estate on which its main raw materials are located and has established an extensive global network of

quarries. As part of its vertically integrated business model, the raw materials from these quarries are used to manufacture primary building materials, such as

aggregates, cement, asphalt, readymixed concrete and concrete products, which are offered directly for sale or integrated into downstream products and

services.

CRH is a significant purchaser of certain materials and resources important to its business, including cement, bitumen, steel, supplementary cementitious

materials and energy supplies, all of which it acquires at market rates. CRH is not dependent on any one source for the supply of these materials and

resources, other than in certain jurisdictions with regard to the supply of gas and electricity.

CRH also utilizes various external suppliers and service providers throughout its business in addition to its internal supply chains, which enables us to

economically source various raw materials, equipment and other inputs and to transport finished product to customers. The Company is committed to

establishing a sustainable and resilient supply chain. The Company takes an active approach to monitoring the resilience of its supply chain and ensures that

it has access to a satisfactory level of required inputs at all times.

Seasonality

Activity in the construction industry is dependent to a considerable extent on the seasonal impact of weather on the Company’s operating locations, with

periods of higher activity in some markets during spring and summer which may reduce significantly in winter due to inclement weather. In addition to

impacting demand for our products and services, adverse weather can negatively impact the production processes for a variety of reasons. For example,

workers may not be able to work outdoors in sustained high temperatures and heavy rainfall and/or other unfavorable weather conditions. Therefore, financial

results for any particular quarter do not necessarily indicate the results expected for the full year. First-half total revenues accounted for 46% of full-year 2023

which is in line with first-half total revenues in 2022.

Competitive Environment

CRH is a market leader in many of the construction markets it operates in across North America and Europe. CRH prioritizes investment in markets with

attractive fundamentals including population and economic growth, which drive demand for construction. Many of the markets in which CRH operates are

highly fragmented, and as a result, CRH products and services face strong competition. The Company’s profits are sensitive to changes in volumes and

prices which are impacted from time to time by market conditions experienced in different markets.

Pricing for products is impacted by macroeconomic conditions, the number of competitors, the degree of utilization of production capacity, the specifics of

product demand, innovation and differentiation, among other factors.

Fragmented markets continue to offer focused growth opportunities for CRH. Similarly, competitors may seek to expand their existing positions or enter new

markets and the Company may experience competition for potential acquisitions identified by CRH management.

CRH Form 10-K 7

3