EUROPEAN

ECONOMY

Economic and

Financial Aairs

ISSN 2443-8030 (online)

Leonor Coutinho, Julien Castiaux,

Jean-Charles Bricongne

and Nicolas Philiponnet

ECONOMIC BRIEF 038 | SEPTEMBER 2018

Housing Market

Developments

in Cyprus

EUROPEAN ECONOMY

European Economy Economic Briefs are written by the staff of the European Commission’s Directorate-

General for Economic and Financial Affairs to inform discussion on economic policy and to stimulate debate.

The views expressed in this document are solely those of the author(s) and do not necessarily represent the

official views of the European Commission.

Authorised for publication by Servaas Deroose, Deputy Director-General for Economic and Financial Affairs.

LEGAL NOTICE

Neither the European Commission nor any person acting on behalf of the European Commission is responsible

for the use that might be made of the information contained in this publication.

This paper exists in English only and can be downloaded from

https://ec.europa.eu/info/publications/economic-and-financial-affairs-p

ublications_en.

Luxembourg: Publications Office of the European Union, 2018

PDF ISBN 978-92-79-77367-9 ISSN 2443-8030 doi:10.2765/600058 KC-BE-18-006-EN-N

© European Union, 2018

Non-commercial reproduction is authorised provided the source is acknowledged. For any use or reproduction

of material that is not under the EU copyright, permission must be sought directly from the copyright holders.

European Commission

Directorate-General for Economic and Financial Affairs

Housing Market Developments in Cyprus

Leonor Coutinho, Julien Castiaux, Jean-Charles Bricongne and Nicolas Philiponnet

Summary

This study analyses demand, supply and price developments in Cyprus, in the run-up to its banking

crisis and the early years of the recovery, analysing also new information on prices in levels. It further

looks into alternative models to forecast house price inflation in Cyprus taking into account particular

country characteristics and developments. Although there are many difficulties with this exercise,

related to data availability, this analysis constitutes a first step in creating a database of relevant data

and understanding the empirical correlation between potential explanatory variables and house prices

trends. There appears to be a correlation between house prices and purchasing capacity, deposits,

foreign sales, housing stocks, and NPLs. The presence of higher NPLs in particular appears to drag

house prices down. High NPLs not only indicate credit tightening, but they also reflect pressure on

households and businesses for real estate asset disposal as a mean to assist deleveraging, and therefore

an ensuing increase in real estate supply.

Acknowledgements:

We would like to thank the staff of the Central Bank of Cyprus, in particular

Pany Karamanou and George Kyriacou, for useful comments and suggestions. We also thank

Magdalena Morgese, David Lopes, and Norbert Gaal for their comments and suggestions, which

contributed to improve the paper significantly. All remaining errors are the authors' only.

Contact

: Leonor Coutinho, European Commission, Directorate-General for Economic and Financial

Affairs, Macroeconomic Imbalances and Adjustment,

leonor.coutinho@ec.europa.eu.

EUROPEAN ECONOMY Economic Brief 038

European Economy Economic Briefs Issue 038 | September 2018

Introduction

Understanding the developments in the Cypriot

housing market can help to better assess the

country's adjustment after the crisis. This paper

discusses demand, supply and price developments in

Cyprus in order to shed light on the importance of

this sector for the unwinding of imbalances in the

financial and non-financial private sector. It further

analyses the determinants of house prices in Cyprus,

to help predict future developments, emphasising the

impact of legacies from the crisis, particularly non-

performing loans.

The Cypriot housing market was severely

affected by the global financial crisis and

subsequently by its own banking and sovereign

debt crisis. Housing sales fell by 60% between the

2007 peak and 2009, as the global financial crisis

unfolded. Still, sales to residents held up relatively

well up to 2012, cushioned by a significant

expansion of mortgage credit to Cypriot households.

As credit expansion stalled in 2012, housing sales

declined further. In 2015 housing sales amounted

roughly to 20% of the 2007 peak.

The foreign segment of the housing market

continues to be of importance to Cyprus despite

its declining share in sales during the crisis. The

crisis affected most significantly property sales to

non-residents, which had doubled in size between

Cyprus' EU membership in 2004 and the 2007 peak,

according to data on registered sales contracts by

nationality. With the global financial crisis, foreign

sales dropped by more than 80%, and continued to

fall further to stand at about 10% of their 2007 peak

level in 2015. In 2016 this segment represented

about 25% of the total market sales.

The combination of depressed sales and excessive

stock accumulation led to a sharp fall in prices, a

decline of about 30% between 2008 and 2015. In

other European countries like Spain and Ireland the

house price correction was even more pronounced

(about 35% and 50% respectively) but it is difficult

to compare the dynamics across countries due to

catching-up effects and differences in the pre-crisis

valuation. According to the central bank of Cyprus

index of housing prices, published also by the ECB,

house prices continued to fall in 2016, but at a more

moderate pace (-1.4%), showing signs of recovery in

2017.

In the context of a high proportion of loans to

households, developers and SMEs, which are

secured by real estate wealth and are non-

performing, the behaviour of house prices can be

of key importance. In Cyprus a large proportion of

loans is collateralised by real estate property. As the

value of this collateral declined banks needed to

scale up provisions for losses, particularly in the

context of a high, even though declining, ratio of

non-performing loans. Also, as property prices

declined, incentives for strategic default increased

among borrowers, especially when non-primary

residences are at stake.

1

The recovery of collateral

prices can increase the range of available

restructuring options as it reduces the amount of

"under-water" mortgages (i.e. with outstanding

principal above the market value of the house), and

facilitates asset disposal as a deleveraging tool for

both households and businesses. It is important to

note also that in Cyprus, loans to SMEs are often

secured by households' real estate.

To help gauge the medium term prospects of this

market in Cyprus, the remainder of this note

discusses in more detail demand, supply and price

developments since EU accession and proposes

alternative models for house price forecasting

focusing on the role of credit and non-performing

loans in particular. Section 1 describes demand

developments and the main variables affecting

demand for housing; section 2 analyses supply

developments; and section 3 discusses the ensuing

price dynamics. In section 4 the paper proposes

alternative models for house price forecasting in

Cyprus and a method to combine forecasts given

model uncertainty and small sample biases. Section

5 concludes.

Main demand developments

The average purchasing capacity of Cypriot

households fell, in line with the reduction of

disposable income during the crisis, but

recovered somewhat since 2014, supported by a

significant reduction in interest rates. The

purchasing capacity of Cypriot households (see

definition in Annex 1) increased significantly in the

run-up to euro area accession in 2004, not only due

to high annual rates of nominal GDP growth but also

to the downward convergence of interest rates

towards euro area levels (Graph 1). Between 2010

and 2014, as the sovereign debt crisis unfolded in

Europe, the purchasing capacity of Cypriot

2

European Economy Economic Briefs Issue 038 | September 2018

cal

culations

T oyment rate increased significantly

Graph 3: Credit standards on house purchases

Source: European central bank lending surv y.

Adding to the demand constraints, access to

ho

useholds fell, in line with low nominal growth and

relatively high interest rates. The downward trend

stalled in 2014 with a recovery initially aided by a

reduction in interest rates and later supported by

economic growth. Deposits, which are not included

into the concept of purchasing capacity, but can be

used as a proxy for savings, fell significantly

between mid-2012 and 2014 but have since

stabilised (Graph 2).

Graph 1: Average purchasing capacity of Cypriot

households

Source: Source: Eurostat, Central Bank of Cyprus and

own calculations

Note: Household disposable income is calculated using

quarterly data on compensation of employees and the

annual share of compensation in disposable income

interpolated.

Graph 2: Average household deposits

Source: Eurostat, Central Bank of Cyprus and own

he unempl

with the crisis, from a pre-crisis rate of 4% to

around 15% in 2015, and although it has receded it

still remained close to 10% in 2017, with a relatively

high incidence of young and long-term

unemployment. Despite the fact that average

purchasing power is recovering, this could be

masking significant inequality among households, as

unemployment can constrain the number of

households able to obtain credit and buy or build a

house, especially among the young. This problem,

however, is mitigated in Cyprus by a high incidence

of housing gifts, from parents to children,

traditionally upon marriage, documented in previous

Cypriot household surveys.

2

Housing gifts are also

in line with the wide income dispersion among home

owners in Cyprus, found in the more recent 2013

Household Finance and Consumption Network

(HFCN) survey.

(supply)

e

Data only available from 2009Q2.

credit was signific

antly tightened, in view of the

very high rates of non-compliance. Despite the

significant reduction in lending rates, which has

supported the purchasing capacity of households

through the crisis, access to credit has been tightened

in Cyprus, especially since end-2011, alongside a

mounting ratio of non-performing loans. Although

further tightening seems to have ceased, according

to both backward looking and forward looking bank

lending survey indicators, a significant relaxation

has not yet been observed (Graph 3), leading to low

flows of additional credit for housing purchases.

3

This has inhibited the ability of liquidity strapped

3

European Economy Economic Briefs Issue 038 | September 2018

Graph 4: Housing sales by residency and housing

Source: Cyprus Ministry of Finance and Central Bank of

ow inflation depressed the growth of nominal

Graph 5: Bank liabilities of Cypriot Households

Source: Central bank of Cyprus and Eurostat

tion

The non-resi

dent segment of the housing market

ho

useholds to purchase properties, despite

reasonable income flows on average. As a result,

housing sales to resident households fell, in line with

the tightening of credit both in 2007-2008, with the

global financial crisis, and in 2011-2013, with the

sovereign debt crisis (Graph 4). Since 2015 sales

have increased from very low levels, but according

to the Cyprus developers' association a significant

number of transactions were in cash and have also

included debt-to-asset swaps between mortgage

debtors and banks, with the number of new

mortgages remaining very limited well into 2017

(Graph 4).

4

credit to residents

Cyprus.

Note: Sales data from 2004 to 2007 have been

interpolated from annual data.

L

GDP, slowing down the

process of household

deleveraging, which would help to rebalance the

credit market. In Cyprus, housing loans to resident

households represent about 50% of all bank loans to

resident households, and about 80% of housing and

consumer loans (excluding "other lending" to

households). Up to 2013Q1, the stock of housing

loans had been increasing on a continuous basis to

reach about 66% of GDP. Since the second quarter

of 2013, alongside the more significant tightening of

credit supply conditions, the stock has started to fall,

but due to moderate nominal GDP growth,

households have not managed to reduce significantly

their housing debt stock as a share of GDP (Graph

5). On this front, a return to moderate rates of

inflation, which in the first seven months of 2017

has reached 1% after four years of consecutive

decline, helps to support nominal incomes and

accelerate the deleveraging process. Still, despite the

accelerating growth, non-performing loans in the

household sector remain very high (around 50% of

total household loans in 2017). Private sector, non-

performing loans (including households, see

Graph 5) increased significantly as the crisis

unfolded. Some of the increase was also due to a

change in the definition of non-performing loans

which became significantly stricter in 2013Q2, with

another subsequent revision in 2014Q4.

5

N

ote: dashed lines mark changes in the defini

contracted significantly with the global financial

crisis of 2007-2008 and, although sales started to

increase from very depressed levels, the profile of

buyers has changed. Sales of property to

foreigners, which represented about 50% of total

sales between 2004 and 2008, contracted from

around 11 000 a year in 2007 to around 1 000 in

2013, while sales to locals contracted from about the

same number in 2007 to a trough of close to 3,000 a

year in 2013. Both segments experienced some

recovery since, to annual values of around 1 800 and

5 250, for the foreign and local market respectively

in 2016 (Graph 4), with the local market

representing about 75% percent of the market in

2016. Housing loans to non-residents represented

only about 11% of the total housing credit and have

been on a declining trend since 2012Q2, with this

decline having accelerated since 2015Q2. According

to the authorities the profile of foreign buyers has

changed since the crisis, with British buyers being

replaced with buyers from Russia, Asia and the

4

European Economy Economic Briefs Issue 038 | September 2018

Proble

ms related to the issuance and transfer of

Rental yields remained relativel

y low despite the

Main supply developments

Between 2008 and 2011 the growth of the housing

Graph 6: Housing stock and number of households

Source: Cystat and Eurostat. The number of households

Mid

dle-East, who are attracted by residency permits

offered by Cyprus under certain conditions that

include the purchase of property. According to the

developers association, transactions in this segment

of the market since 2015 included an important

number cash transactions and prices are relatively

high due to the higher income profile of current

foreign buyers.

6

title deeds have the potential to deter investors

and aggravate credit market distortions. There is

an increased awareness among Cypriots and foreign

buyers of the delays in issuing and transferring title

deeds, and of the fact that many properties now

available for sale may be encumbered by mortgages

and/or memos from other creditors, including the

State. A significant number of buyers in Cyprus, the

so called “entrapped” buyers, have paid the full price

for their properties but saw the transfer of the title to

their names blocked by existing encumbrances on

the property, which relate to developers loans and

other debts, including tax debts. Introduced in 2015,

the “trapped buyers' law” was designed to protect

trapped buyers by releasing the property they have

purchased from the developer’s obligations to their

lenders, enabling the buyer to obtain the title deed

for the property.

7

Further, a decree issued by the

Interior Minister in 2016 authorises local authorities

to excuse predefined planning irregularities on

properties, making it this way possible to speed up

the issuance of title deeds when no title had yet been

issued.

8

Still, some 34,000 title deeds were still

pending issuance by mid-2017.

9

More importantly,

there is no effective system to guarantee that, in

future transactions, the money paid by the buyer will

be used to fulfil the obligations of the seller towards

its lender and remove any encumbrances on the

property, as there is no notary system in Cyprus as in

other European countries.

significant correction in prices, depressing the

investment value of real estate. According to the

Royal Institution of Chartered Surveyors (RICS)

10

,

average gross yields in Cyprus in 2016Q4 stood at

4% for apartments, 2.1% for houses, 5.3% for retail,

4.4% for warehouses, and 4.6% for offices. The

stabilisation in capital values and rents keept

investment yields relatively stable but at low levels.

Mortgage rates in Cyprus were well above 4%

before March 2015 but have since declined to stand

at around 3% in 2016. This means that local

borrowing to invest in an apartment to rent it out has

only become a barely profitable investment in 2016,

while the same type of investment on a house

continued to be unprofitable. At the same time,

foreign property investors with a view to rent are

unlikely to be attracted by the Cypriot market at

current yields, which according to RICS stand below

overseas yields in 2016. This may be related to

frictions in Cypriot house market (see Box 1) which

may have maintained rental yields depressed on

average.

stock exceed

ed sales by significant amounts,

creating an excess supply which could take time

to be reabsorbed by the market. There are

indicators of an accumulated excess supply of

housing in Cyprus (Graph 6). Between 2004 and

2008 the housing stock grew rapidly and production

took time to adjust to the sharp fall in sales in 2008

and 2009. Just taking the difference between the

housing stock and sales between 2004 and 2015, an

accumulated stock of about 10 000 dwellings can be

identified, which at the construction/sales rate of

2015 will take up to 2018 to be absorbed by the

market. Another indicator of a current excess supply

comes from comparing the growth rate of the

housing stock to the growth rate of the estimated

number of households. This comparison indicates

that dwellings per household increased by about

20% from 1995 to 2015, from 1.2 to 1.4.

eq

uals population divided by the average size of

households. Before 2005 the average size of households

was kept at the 2005 level due to unavailability of data.

5

European Economy Economic Briefs Issue 038 | September 2018

Source: Eurostat

on-housing construction investment also fell

In response to the excess supply of housing,

construction

activity contracted significantly

following the peak in 2008, but construction

output has started to recover. Activity in the

construction sector has dropped by more than 70%

between 2008 and 2015. The sector was the hardest

hit by the crisis. Compared to other sectors,

construction has the largest share of bank loans to

total bank lending to nonfinancial corporations

(about 28%), and has the highest ratio of non-

performing loans (about 75%). Labour shedding in

the sector was limited and profit margins have

shrunk significantly.

11

Since mid-2015 the real

GVA of the sector started to grow again,

moderately. In addition, cement sales and building

permits have also started to increase (Graph 7).

12

Graph 7: Indicators of housing supply

N

signific

antly, especially since 2011 when credit

tightening was more visible, and and may remain

constrained by the private and public debt

overhang. Excessive debt works as a tax on

investment as its returns have to be used to pay out

old debt.

13

This creates a disincentive for

overleveraged borrowers to invest, while at the same

time prevents them to earn more in the future and

pay-off the debt. This is the so-called debt-overhang.

As evidence of this effect, total investment in

Cyprus fell from about 27% of GDP in 2008 to

about 14% in 2015, and non-dwelling construction

investment (other buildings and structures) fell from

about 7% of gross GVA to about 4% in the same

period (Graph 8).

Graph 8: Construction Investment by type

Source: Eurostat

House price developments

Alternative residential price indexes indicate that

the market reached a turning point. There are

three main indexes for Cypriot residential prices, the

Eurostat index of residential prices (compiled by

Cystat), the ECB index of residential prices

(compiled by the Central Bank of Cyprus), and the

RICS index of house prices (Graph 9). According to

the Eurostat index, residential price inflation has

been low but positive on average since 2014Q3.

According to the ECB index, house price inflation

continued to be negative until 2016Q1, but the pace

of price decline has decelerated progressively since

2014Q3, to stand at around -1.6%. A similar pattern

is shown by the RICS index, but the deceleration of

the fall in prices has been faster according to this

index, and in 2016Q1 prices were virtually stable

(y–o–y inflation of 0.6% for houses and -0.2% for

flats).

14

All in all, indications are that prices hovered

around a turning point in 2016-2017.

The closing down of the gap between new houses

and sales is also indicative of a turning point. The

ratio between new housing and sales is generally a

good leading indicator of price developments as it

points out a change in the balance of power between

buyers and sellers, to the detriment of the former

when the ratio is declining. In Cyprus this ratio

increased significantly in 2008 and 2009 but started

to decline since, approaching 1 in 2013, and going

below 1 thereafter (Graph 10).

6

European Economy Economic Briefs Issue 038 | September 2018

Graph 9: House price indexes, alternative sources

Source: Eurostat, ECB, RICS

Graph 10: Change in dwelling stock and sales

Source: Cystat and Eurostat.

Real house prices increased virtually as much as

nominal prices up to 2008 but on the downward

adjustment phase, they have been supported by a

period of negative inflation. The deflator of private

consumption is the variable generally used to deflate

house prices. This deflator has been relatively stable

in Cyprus. Since 2014 the negative growth in this

deflator has kept the decline in real house prices

contained. But this effect is winding down as the

deflator stabilises. As inflation picks-up in Cyprus,

the recovery of nominal house prices will have to

accelerate in order for an increase in real terms to

materialise.

Information on house prices in levels obtained

from alternative sources indicates that the house

price to income ratio remained relatively high in

2016. Information on house prices in levels, when

available, can be helpful to access how much

adjustment has taken place. Graph 11 shows Cypriot

house prices in levels as a ratio to gross disposable

income of households. One data point has been

tentatively calculated from alternative sources and

then extrapolated to other years using either the ECB

price index, which is also used later on in the

econometric analysis, or alternatively the Eurostat

price index (see Annex 1 for the methodology). The

price information in levels shows that in 2016, the

house price-to-income ratio stood between 10 and

17, approximately, while according to the literature

the prudency level for this ratio is below 10.

15

This

information signals that to maintain houses

affordable house price growth going forward should

still be contained and not exceed the growth rate of

household gross disposable income.

Graph 11: House price-to-income ratio,

alternative sources for house prices in levels

Source: Household Finance and Consumption Survey

(HFCS), RICS, ECB, Eurostat and own calculations

explained in Annex.

Modelling Cypriot house prices

The empirical model

A simple way to forecast Cypriot house prices is

to relate them to purchasing capacity as previous

studies have done for other countries. The house

price that households can afford with credit is a

function of their disposable income, the interest rate

on housing loans, and the loan maturity. An increase

in disposable income will increase the size of the

payments that households can afford each period,

while higher interest will lower the present value of

these payments. Longer loan maturities allow for

more payments to enter into the calculation,

increasing the affordable price. All these effects

have been summarised in the literature by a single

variable, known as purchasing capacity, constructed

as follows:

16

7

European Economy Economic Briefs Issue 038 | September 2018

CAP

=

(

)

8

+

(

)

+⋯

(

)

=

(

)

(1)

This purchasing capacity represents the value of a

loan at fixed interest rate (i

t

) and maturity T that a

household can sign up to if it devoted to its payment

a constant fraction (k) of its income, where Y

t

is

disposable income per household. Abstracting from

credit frictions (such as down-payments, collateral,

and other credit constraints) and assuming that

demand and supply in the property market balance

out, a simple long-run model relating house prices

t emerges (in logs):(P

t

), o purchasing capacity

ln

(

)

= + ln(

) (2)

17

In Cyprus t

he purchasing capacity of residents

alone may not be the best indicator of the buyers'

purchasing capacity up to 2008, as sales to

foreigners represented about 50% of the market, but

data constraints make it difficult to capture the effect

of foreign buyers in the market. The two main

foreign markets for Cyprus are the UK and Russia,

but considering a weighted average of the domestic

purchasing capacity and that of the UK in euros does

not improve the results (the required data to

construct a Russian purchasing capacity is not

available). Information on sales to foreigners could

also be used but the data only exists from 2004 on an

annual basis and from 2008 on a quarterly basis,

reducing the sample considerably.

Household deposits may also be important to

determine housing demand in Cyprus, as it is a

social custom for parents to save to provide housing

to children. In Cyprus, a measure of purchasing

capacity of households based on income may not be

the best indicator of affordability, as it has been a

social custom for parents to save up to provide

housing to their children, typically when they marry.

As other savings instruments are less developed in

Cyprus, household deposits could also be a good

indicator of housing demand.

Given the importance of the foreign segment of

the market in the case of Cyprus it is also

important to test for the impact of developments

in sales to foreigners. While the foreign segment of

the market was in great part a driver of the boom in

construction investment up to 2007, it is also greatly

responsible for the burst of the bubble. Also, to the

extent sales to foreigners yield now a better yield,

the recovery of the foreign market may also play a

significant role in explaining the recovery. The

number of sales contracts by nationality (foreigners

versus Cypriots) is available from the Department of

Land Surveys of Cyprus. Between 2004 and 2007

the data is annual and has been interpolated to

quarterly, using the seasonal pattern of the quarterly

data, available from 2008 to date.

18

Both the

numbers and the share in total sales have been

considered in the analysis.

A range of other variables may also contribute to

explaining house price developments, including

indicators of housing over-/under- supply. Data

on the house (dwellings) stock is only available on

an annual basis but can be interpolated using

investment in dwellings. The ratio of the housing

stock to population, which has been found to be

significant for other studies, can be used as an

indicator of over/under supply.

19

An increase in this

variable should signal a shift in the bargaining

power towards buyers and point towards a reduction

in prices.

Credit market indicators may also play a role but

the data has its limitations. Conditions in the credit

market can also be important to explain house price

developments as liquidity strapped households may

not afford to buy a house, even if their income is

relatively high, without having access to credit.

20

However, the ECB bank lending survey indicator of

credit tightening has a very short sample in the case

of Cyprus and would limit the estimation sample

considerably. It is possible to use instead credit to

households, which is available for a reasonable

number of years, with the caveat that this variable is

likely to be endogenous to house prices when

housing loans represent a large part of total loans.

This variable has nevertheless proved to be a useful

indicator of house price developments in other

studies, and the endogeneity problem can be

addressed to some extent with the estimation

methodology. An alternative variable, which is

highly correlated with credit conditions, both as a

driver and as a consequence is the ratio of non-

performing loans (NPLs) to total loans. Since in

Cyprus there have been changes in the definition of

NPLs over the sample, we use a spliced series over

the period from 2005Q1, with its caveats in mind.

21

Finally, the unemployment rate can also be used

to proxy for demand constraints.

22

A higher

unemployment rate can signal more inequality in the

distribution of income among households. It also

indicates a higher probability of getting unemployed,

increasing uncertainty over future income flows.

European Economy Economic Briefs Issue 038 | September 2018

9

This leads households to postpone purchasing

decisions and banks to tighten credit supply.

Estimation results and price forecasts

There are limitations in the analysis in terms of

data availability and sample size, but model

estimates can give insights on the correlation

between house price developments and the

various explanatory variables. Alternative versions

of the housing price model have been estimated

using an error correction specification that implies

that house prices can temporarily deviate from the

long-term model described in equation (2) but will

return to it after some time. Rather than proposing a

model, the aim of the exercise is to document the

properties of alternative models, and highlight the

variables that appear to be empirically more

important for the analysis. The estimation uses a

two-step approach, with the long-term model

estimated first using the Dynamic Ordinary Least

Squares (DOLS) methodology, and the short-run

equation, determining the adjustment to the long-

run, estimated conditional on the DOLS parameters

(Equation 3).

23

We also account for endogeneity by

assuming that it takes about 4-quarters for the

explanatory variables to affect housing prices.

24

The

dependent variable is the log change of the house

price index of the ECB. The purchasing capacity

ap scrib in Appendix. variable (c in logs) is de ed the

∆

=

(

)

+

∑

∆

+

∑

∆

+

(3)

Purchasing capacity alone cannot explain house

price trends in Cyprus. This could be explained to

some extent by the relatively short sample available

(from 2002Q2 on was used for the estimation),

which may not allow identifying a stationary long-

term relationship between house prices and

purchasing capacity, but may also be due to the

importance of additional variables in explaining

house price trends. Given the relatively short sample

it is not easy to estimate a very encompassing model

without running into problems of instability, hence

additional variables have been tested in alternation.

Adding additional variables to the analysis does

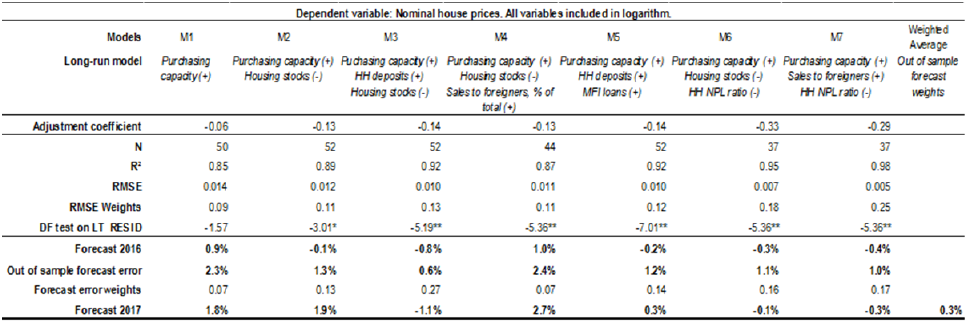

improve the properties of the model. Table 1

summarises the estimation results for alternative

models estimated (selected on the basis of their

RMSE, with the exception of model 1 which was

retained for comparison with the literature), while

less-performing variations of these specifications are

shown in the Appendix. Model 1 does not work

well in the sense that the long-term relationship

estimated is not stationary and therefore the

properties of inference based on stationarity

assumptions do not hold. It has been included in the

table to show that purchasing capacity alone tends to

over-predict house price growth in Cyprus.

Including housing stocks stabilises the long-term

relationship but points towards a slower recovery

(Models 2 and 3). Including the unemployment rate

yields implausible results (the models are shown in

the appendix).

25

Table 1: House price models and forecasts

Source: Own estimations. Models include a constant in the cointegrating vector and four to six lags of the explanatory

variables. Dummies for 2004 Q1 and 2008Q1 (membership in EU and EMU, respectively) are significant and have been

included as explanatory variables. The Johansen cointegration test indicates 1-cointegrating equation among the variables

(results available upon request) Except for disposable income and unemployment, for which the Commission forecasts have

been used, other explanatory variables are forecasted using an ARIMA extrapolation. ** Rejects the hypothesis that the

residual in I(1) using Phillips and Peron (1988) critical values at 5% significance.

European Economy Economic Briefs Issue 038 | September 2018

Including in the analysis indicators of excess supply

or of credit conditions yields a more protracted

recovery of house prices. The most pessimistic model

overall is that which includes the ratio of housing

stocks to the population combined with purchasing

capacity and deposits (Model 3). This is however the

model that yields the lowest out of sample forecast for

2016. Taking into consideration credit conditions

(proxied by the NPL ratio) developments are similar,

but more optimistic for 2017 (Models 6 and 7).

Overall, averaging out the results weighted by the

inverse of out of sample forecast error, yields a

prediction of close to flat prices in 2017 (0.3%).

1

Weighing by the inverse of the RMSE the forecast

for 2016 gives a similar, slightly higher forecast

(0.5%).

Conclusion

There are many difficulties in estimating a house

price model for Cyprus, but the analysis of the data

can give some insights on the relative importance of

possible explanatory variables. The existing data has

many limitations in terms of sample size, frequency,

changes in definition and inconsistencies across data

sources. This study is a first step in creating a database

of relevant data and understanding the empirical

correlation between potential explanatory variables and

house prices trends. There appears to be a correlation

between house prices and purchasing capacity,

deposits, foreign sales, housing stocks, and NPLs.

26

The presence of higher NPLs in particular appears to

drag house prices down. High NPLs not only indicate

credit tightening, but they also reflect pressure on

households and businesses for real estate asset disposal

as a mean to assist deleveraging, and therefore an

ensuing increase in real estate supply.

Indicators point to 2017 as a turning point, but the

recovery is likely to be protracted. Developments in

the purchasing capacity of households, measured by

the present value of their income streams, everything

else constant, indicate that there are conditions for

house prices to increase relatively fast. However, when

other indicators are taken into account including

household deposits, unemployment, credit conditions,

and housing stocks the results are more mixed. In

particular, when credit and excess supply indicators are

1

included in the analysis, the signs are of a more

protracted recovery.

In Cyprus there has been a vicious loop between low

house prices, NPLs and low credit to the economy,

which will be difficult to break without ensuring that

proceeds from sales are channelled to reducing the

NPL stock. Credit for housing has been significantly

curtailed in Cyprus. Despite that sales have been

steadily increasing, even though the numbers are still

much lower than previously. Many of these sales are

undertaken in cash, and currently in Cyprus there is no

means to ensure that the proceeds are used to pay the

non-performing loans of the seller if applicable. If the

proceeds are used instead to finance new buildings, this

will protract the absorption of the existing stock (most

of it encumbered), maintain house prices low at least in

some areas, and will delay the balance sheet adjustment

of banks. This adjustment is essential for credit to be

channelled to productive investments that can secure

the growth potential of the economy.

Higher rental yields would also assist deleverage by

increasing the investment value of housing.

Removing existing obstacles for further development

of the rental market would help increase rental yields

and increase the investment value of housing. With the

boom in tourism currently experienced in Cyprus,

demand for renting has increased, particularly in

coastal areas. An excess of unregulated supply, in

terms of quality and environmental impact, can also be

detrimental for the market, hence attention must be

paid to how this market evolves. In other areas, rent

control and the underdevelopment of speedy channels

for resolving disputes can create various distortions

that may also require policy action.

10

European Economy Economic Briefs Issue 038 | September 2018

References

Bricongne, J-C, Turrini, A., and Pontuch, P. (2017), "Assessing House Prices: Insights from HouseLev, A New

Dataset of Prices in Levels", European Commission Discussion Paper, forthcoming.

Engle, R.F., Granger, C.W.J. (1987), Co-integration and error correction: Representation, estimation and testing.

Econometrica 55 (2), 251-276.

ECB (2013), "Dwelling Stock in the euro area - new data from the Eurosystem Household Finance and

Consumption Survey", ECB Monthly Bulletin July, Box 7, pp. 51-55.

https://www.ecb.europa.eu/pub/pdf/m

obu/mb201307en.pdf

European Commission (2016) "Cyprus 1st Post Programme Surveillance Report",

Autumn, https://ec.europa.eu/info/publications/economy-financ

e/post-programme-surveillance-report-cyprus-

autumn-2016_en

European Commission (2016a), Country Report for Cyprus, "Private Indebtedness", chapter 23, 23-

31. https://ec.europa.eu/info/publications/2016-european-semester-country-report-cyprus_en

Guiso, L., Sapienza, P., and Zingales, L. (2013), "The determinants of attitudes toward strategic default on

mortgages", The Journal of Finance, 68(4), 1473-1515.

Halliassos, M., Karamanou, P., Ktoris, C., and Syrichas, G. (2008), "Mortgage debt, social customs, and financial

innovation", Central Bank of Cyprus, Working Paper 2008-2.

INSEE (2008), Box "Éclairage : modélisation des prix immobiliers en France", in Conjoncture

France, http://www.insee.fr/fr/indicateurs/analys_

conj/archives/mars2008_f3.pdf

Iossifov, P., Cihak, M., and Shanghavi, A. (2008), "Interest Rate Elasticity of Residential Housing Prices", IMF

Working Paper No 08/247, International Monetary Fund.

Krugman, P. (1988), “Financing versus Forgiving Debt Overhang”, Journal of Development Economics 29, 253-

268.

McQuinn, H. and O'Reilly, G. (2008), "Assessing the role of income and interest rates in determining house

prices", Economic Modelling 25, pp. 377-390.

Muellbauer, J., and Murphy, A. (1997), "Booms and busts in the UK housing market", Economic Journal, Vol.107

(445), pp.1701-27.

OECD (2004), Economic Surveys:Netherlands.

OECD (2004a), Economic Surveys:Spain.

OECD (2005), Economic Surveys:Ireland.

Stock, J. and Watson, M. (1983) "A simple estimator of cointegrating vectors in higher order cointegrating

systems", Econometrica 61, 783-820.

Tsatsaronis, K. and Zhu, H. (2004), "What drives house price dynamics: cross-country evidence", BIS Quarterly

Review.

11

European Economy Economic Briefs Issue 038 | September 2018

12

Box 1: THE CYPRIOT RENTAL MARKET

The Cypriot rental market is a dual market where there are two types on tenancies, one liberalised and

one for which rent control applies. The “statutory” tenancy applies to properties, residential or business,

completed by the 31st of December 1999 and situated within the “controlled areas” determined by the Rent

Control Law (23/1983). Statutory tenants, who must be EU citizens who are residents in Cyprus, cannot be

evicted except in certain circumstances provided by law, even if the rental contract has expired, and increases

in the rent are regulated by law. In such cases, the owner has to proceed through the Rent Control Court to

repossess his property. All the other tenancies, remain contractual tenancies and do not fall under the

protection of the Rent Control Law, but are subject to the agreement made by the parties. Usually in such

tenancies, the tenant remains in possession of the property only during the lease period unless the tenancy is

renewed or extended. If the tenant does not leave after the regular end of the tenancy, then the tenancy

becomes a periodic tenancy, and both landlord and tenant should give at least a one-month notice for its

termination. Any claims in relation to a contractual tenancy fall under the jurisdiction of the District Court.

Rent controls make a number of properties less attractive for investors, lowering their value and

liquidity. The Rent Control Law (23/1983) allows for an agreed increase of no more than 14 % of the existing

rent and only after two years have passed from the date of the last application or the date of the last voluntary

increase. If the tenant refuses to pay the increased rent, the Rent Control Court will determine a “reasonable

rent”, taking into account the official value, and factors such as age, size, location and condition of the

dwelling. This inflexibility and reliance on the courts makes it less attractive for owners to invest in

renovation and lowers the investment value of properties in Cyprus.

In the Cypriot rental market all disputes have to be resolved through the currently relatively inefficient

court system, potentially making it less attractive for investors. Disputes regarding rent increases and

evictions in Cyprus are currently settled through the courts. In the case of evictions, if a tenant refuses to

return the dwelling despite the fact that landlord has given a proper notice, the remaining option for the

landlord is to file a court action asking for the return of the dwelling. Cypriot procedural law does not provide

for any accelerated form of procedure used for the adjudication of tenancy cases. Mediation and other

alternative dispute resolution are rarely used, mainly due to their recent introduction into the Cypriot legal

system (Law 159 (I)/2012). It is also worth noting that Cypriot law does not provide for any institutions to

which the tenant may refer to in order to have his rights clarified/protected.

European Economy Economic Briefs Issue 038 | September 2018

Annex 1

Table A1: Alternative house price models and forecasts

Additional Models M8 M9 M10 M11 M12 M13

Long-run model Puchasing capacity (+)

HH deposits (+)

Purchasing capacity (+)

Unemployment rate (-)

HH deposits (+)

Unemployment rate (-)

HH deposits (+)

MFI loans to HH (+)

Purchasing capacity (+)

Deposits (+)

Sales to foreigners (+)

Purchasing capacity (+)

HH Deposits (+)

Sales to foreigners, %

of total (+)

Adjustment coefficient -0.10 -0.09 -0.07 -0.11 -0.20 -0.18

N 52 52 52 52 44 44

R² 0.88 0.87 0.86 0.90 0.91 0.89

RMSE 0.013 0.014 0.014 0.012 0.009 0.010

DF test on LT RESID -2.4 -2.87 -4.57** -5.03** -4.85** - 5.29**

Forecast 2016 1.7% 1.4% 0.1% 0.0% 0.9% 0.8%

Forecast 2017 0.3% 1.6% -1.4% -0.1% 0.8% -0.2%

Dependent variable: Nominal house prices. All variables included in logarithm.

Source: Own estimations. Models include a constant in the cointegrating vector and four to six lags of the explanatory

variables. Dummies for 2004 Q1 and 2008Q1 (membership in EU and EMU, respectively) are significant and have been

included as explanatory variables. The Johansen cointegration test indicates 1-cointegrating equation among the variables

(results available upon request). Except for disposable income and unemployment, for which the Commission forecasts

have been used, other explanatory variables are forecasted using an arima extrapolation. ** Rejects the hypothesis that the

residual in I(1) using Phillips and Peron (1988) critical values at 5% significance.

13

European Economy Economic Briefs Issue 038 | September 2018

Variables used in the analysis

Purchasing capacity: present value of gross disposable income per household taking into account an average mortgage

duration of 25 years, and Cyprus mortgage rates as a discount factor. Households are estimated using population data

and the average number of persons per household. Gross disposable income forecasts are the EC Commission forecasts

for 2016 and 2017 interpolated. Mortgage duration and interest rates are kept constant over the forecast horizon. The

number of households is forecast by extrapolating the trend. Sources: Eurostat and Central Bank of Cyprus.

Household deposits: total household deposits in Cypriot MFIs, divided by the number of households (the latter is

estimated as indicated above). The forecast uses an arima extrapolation. Source: Central Bank of Cyprus long series.

Unemployment rate: Cyprus quarterly unemployment rate, LFS survey. Forecast uses the EC commission forecast for

2016 and 2017, interpolated. Source: Eurostat.

Sales to foreigners: Number of registered sales contracts by nationality (foreigners vs Cypriots). The share is

calculated as the ratio of sales to foreigners over the total sales. It is forecast using an arima extrapolation. Source:

Cyprus department of land surveys.

Housing stocks: Annual stock of housing in Cyprus (available in Cystat) interpolated using investment in dwellings

(constant prices), divided by the population (national accounts). This is forecast using an arima extrapolation. Source:

Cystat and Eurostat.

Household NPL ratio: Ratio of households non-performing exposures to total household exposures (loans) provided

by the Central Bank of Cyprus (spliced series, since 1995), updated to 2016 using data published by the CBC. The

forecast uses an arima extrapolation. Source: Central Bank of Cyprus.

MFI loans: total housing loans in Cypriot MFIs, divided by the number of households (the latter is estimated as

indicated above). The forecast uses an arima extrapolation. Source: Central Bank of Cyprus long series.

14

European Economy Economic Briefs Issue 038 | September 2018

Information on house prices in levels for Cyprus

The Eurosystem Household Finance and Consumption Survey (HFCS) allows to derive a figure for house prices in

Cyprus of 1710€/m2 for 2012 (first wave of HFCS, see also ECB, 2013) and 1483€/m2 for 2014 (second wave of

HFCS). Since richer households tend to be underrepresented in the HFCS survey, it is common practice to weigh

observations by an approximation of the true weight of the share of households in each income bracket. One possible

variable to proxy for these weights in the case of Cyprus is relative electricity consumption, and this proxy has been

used in calculations..

The RICS house price analysis provides figures for houses and flats with a weighted average of 1522.7€/m2 in 2012

and 1280.6€/m2 in 2015. Since the concept of floor area used is the "gross external area" of the property including

external walls (as defined in the RICS’ Code of Measurement Practice 6th Edition), a corrective factor must be used to

convert external walls into useful floor area. When this correction is applied, the values become 2508€/m2 and

2109.2€/m2, for 2012 and 2015, respectively. This is sizeably higher than the figures calculated from the HFCS, but

RICS prices may show an upward bias due to the fact that houses included in the estimations are in urban areas and

apartments in city centres.

Since these different sources are not available for the same period, and since there are two different indexes that may be

used to describe the growth rate of house prices in Cyprus (the Eurostat and the ECB indexes described in the text)

these alternative growth rates can be applied to the alternative sources of prices in levels to allow for comparisons. This

allows observing that the two waves of the HFCS give very similar values for the same year, while the RICS prices are

higher.

An extra source which can be used are realtors' online offers (the sample corresponds to 6321 dwellings offers from

October 2017). Using the number of dwellings by districts obtained from the census data of 2011, this source gives the

weighted average of 2590.8€/m2 and a weighted median of 1840.3€/m2, corresponding to an average surface of

197.1m2 and a median surface of 145m2. The significant discrepancy between the average and the median values

suggests a likely over-representation of prime and luxury goods in the sample of prices advertised online, which would

give an upward bias. In any event, prices from realtors tend to be higher than transaction prices. Extrapolating the prices

in levels obtained from the RICS and the HFCS for 2017, the median price from realtors would lie in between these

estimates, while the average would lie above. Average and median realtors prices correspond to prices to income ratios

of 17.7 and 12.6, respectively.

15

European Economy Economic Briefs Issue 038 | September 2018

16

1

Guiso et al. (2013) show that the willingness to default increases in both the absolute and relative size of the home-equity

shortfall, on others having defaulted previously, and on the probability of becoming unemployed among other things.

2

See Halliassos et al. (2008), who use two waves (1999 and 2002) of the Cyprus Surveys of Consumer Finances, discontinued

since, to document the importance of house gifts in Cyprus (typically from parents to children) to determine the rate of

home ownership in the country.

3

The bank lending survey (BLS) contains 22 standard questions on past (previous three-month period) and expected (for the

following three-month) credit market developments. Overall, the BLS includes 18 backward and 4 forward-looking questions,

in order to capture both recent and expected developments, which make up the backward looking and the forward

looking indexes of credit restrictions.

4

See European Commission (2016).

5

Up to July 2013, the definition of NPLs in Cyprus covered only the value of loans and advances that were not fully covered

by collateral and were in arrears for more than 90 days. After July 2013, the central bank of Cyprus imposed a new, stricter,

definition. The definition changed to include not only loans in arrears for more than 90 days irrespective of collateral, as

called for by the International Financial Reporting Standards (IFRS), but also restructured loans that at the time of

restructuring were either part of NPLs or were in arrears for more than 60 days. The restructured loans had to remain classified

as NPLs for at least six months, or until the largest principal payment for amortised loans had been made or until maturity for

bullet loans. The new definition raised somewhat the volume of NPLs, but provided extra assurance against cosmetic

restructurings or restructurings that are themselves subject to a risk of relapsing into arrears. At the end 2014, this definition

was made stricter by increasing the minimum probation period for forborne loans remaining classified as NPLs from 6 to 12

months and by requiring performing restructured loans presenting arrears greater than 30 days to be classified as NPLs.

6

See European Commission (2016).

7

It restricts the lenders (i.e. the banks) to alienate properties mortgaged by the seller (i.e. the developers) that are currently

under the possession of trapped buyers (Immovable Property Transfer and Mortgage Law Amendment No. 10 of 2015). The

law also gives the discretion to the Director of the Department of Lands and Surveys to exempt, eliminate, transfer and

cancel mortgages and/or other encumbrances applicable on the property and to transfer the title deed to the final buyer.

8

This allows for the issuance of the Certificate of Approval, which is prerequisite for the issuance of a title deed. This measure

offers trapped buyers increased guard against the lender of the seller, since a title deed must exist in order an application

under the provisions of the “trapped buyer law” to be processed. The number of buyers in this situation is uncertain but

according to the Cypriot press ranged around 14,000 by June 2017 (Cyprus property news, 24th June 2017). In May 2017,

courts in Cyprus ruled that provisions of the "trapped buyers' law" were unconstitutional, creating uncertainty on the process.

http://www.news.cyprus-property-buyers.com/2017/06/24/reprieve-trapped-buyers/id=00152584

9

Department of Land Registry statistics cited by Cyprus property news, 24th June 2017. http://www.news.cyprus-property-

buyers.com/2017/06/24/reprieve-trapped-buyers/id=00152584

10

This is the leading professional body for qualifications and standards in land, property, infrastructure and construction. RICS

is headquartered in London.

11

See European Commission (2016a).

12

Building permits are relatively flat because developers have already a portfolio of permits. According to the Cyprus

Developers Association, since there is a long time lag in Cyprus to obtain a building permit (more than 2 years), developers

followed the practice of stocking plots of land, submitting the corresponding building plans for approval well ahead of

demand materialising.

13

See Krugman (1988).

14

http://www.rics.org/Global/Cyprus%20Property%20Price%20Index%20Q1%202016.pdf

15

See Bricongne et al. (2017).

16

See McQuinn, H. and O'Reilly, G. (2008) for the case of Ireland, and INSEE (2008) for the case of France.

European Economy Economic Briefs Issue 038 | September 2018

17

17

Notice that the choice of the constant k serves only to better match the estimated capacity to the level of house prices

and does not have an impact on the relationship between house prices and income capacity.

18

From 2008 onwards the data are actually available on a monthly frequency.

19

See Muellbauer, J., and Murphy, A. (1997) and OECD (2004, 2004a, and 2005).

20

See Tsatsaronis, K. and Zhu, H. (2004) and references therein.

21

The spliced series has been kindly provided by the Central Bank of Cyprus research department.

22

See Iossifov et al. (2008) and references therein.

23

The dynamic ordinary least squares (DOLS) methodology of Stock and Watson (1993) extends the single-equation Engle-

Granger (1987) approach to cointegration to allow for endogeneity within the specified long-run relationships. It adds both

leads and lags of the differenced regressors to the long-run specification to correct for correlation between the error

process and the level regressors.

24

Estimates are not very sensitive to the lag choice.

25

A model including the unemployment rate, purchasing capacity and deposits does not exhibit reversion towards the long-

term trend, as the error correction term in the dynamic model is not significant. The model performs better when purchasing

capacity is excluded. This may be due to a high correlation between the purchasing capacity and the unemployment rate.

26

Notice that only models where a cointegrating relationship between the variables could be found were retained.

EUROPEAN ECONOMY ECONOMIC BRIEFS

European Economy Economic Briefs can be accessed and downloaded free of charge from the following

address:

https://ec.europa.eu/info/publications-0/economy-finance-and-euro-

publications_en?field_eurovoc_taxonomy_target_id_selective=All&field_core_nal_countries_tid_selective=All

&field_core_flex_publication_date[value][year]=All&field_core_tags_tid_i18n=22614.

Titles published before July 2015 can be accessed and downloaded free of charge from:

• http://ec.europa.eu/economy_finance/publications/economic_bri

efs/index_en.htm

(ECFIN Economic Briefs)

• http://ec.europa.eu/economy_finance/publications/country_focus/index_en.htm

(ECFIN Country Focus)

GETTING IN TOUCH WITH THE EU

In person

All over the European Union there are hundreds of Europe Direct Information Centres. You can find the

address of the centre nearest you at: http://europa.eu/contact.

On the phone or by e-mail

Europe Direct is a service that answers your questions about the European Union. You can contact this

service:

• by freephone: 00 800 6 7 8 9 10 11

(certain operators may charge for these calls),

• at the following standard number: +32 22999696 or

• by electronic mail via:

http://europa.eu/contact.

FINDING INFORMATION ABOUT THE EU

Online

Information about the European Union in all the official languages of the EU is available on the Europa

website at: http://europa.eu.

EU Publications

You can download or order free and priced EU publications from EU Bookshop at:

http://publications.europa.eu/bookshop. Multiple copies of free publications may be obtained by contacting

Europe Direct or your local information centre (see http://europa.eu/contact).

EU law and related documents

For access to legal information from the EU, including all EU law since 1951 in all the official language

versions, go to EUR-Lex at: http://eur-lex.europa.eu.

Open data from the EU

The EU Open Data Portal (http://data.europa.eu/euodp/en/data) provides access to datasets from the EU.

Data can be downloaded and reused for free, both for commercial and non-commercial purposes.